Strategies to improve customers’ share of wallet at your bank

Sometimes banks tend to put a lot of emphasis on attracting new customers, but a key way they can improve revenue is by making sure existing customers sign up for new products and services.

by Mayur Vichare

Many people often stick to one or two financial institutions throughout their working life, so it’s not surprising that acquiring new customers is extremely difficult.

Sometimes customers might look at switching to a new bank, but only if there’s a big need for it. If a new customer does decide to join, the onboarding process can end up being quite costly for a bank. For example, it can cost up to $1,500 in the US and $80 in the Philippines to process a new banking customer.

While it’s important to continue attracting new customers, banks should also strongly focus on how they can increase the number of products each existing customer has.

Once you have a deep understanding of your customer’s needs you can then begin to offer them targeted products and services to increase your revenue. The aim is to offer an experience and products that leave your customers satisfied, loyal, and recommending your bank to others.

I will take you through a number of strategies my team of consultants at Backbase considers when driving an improved share of wallet.

Analyze what products existing customers are using

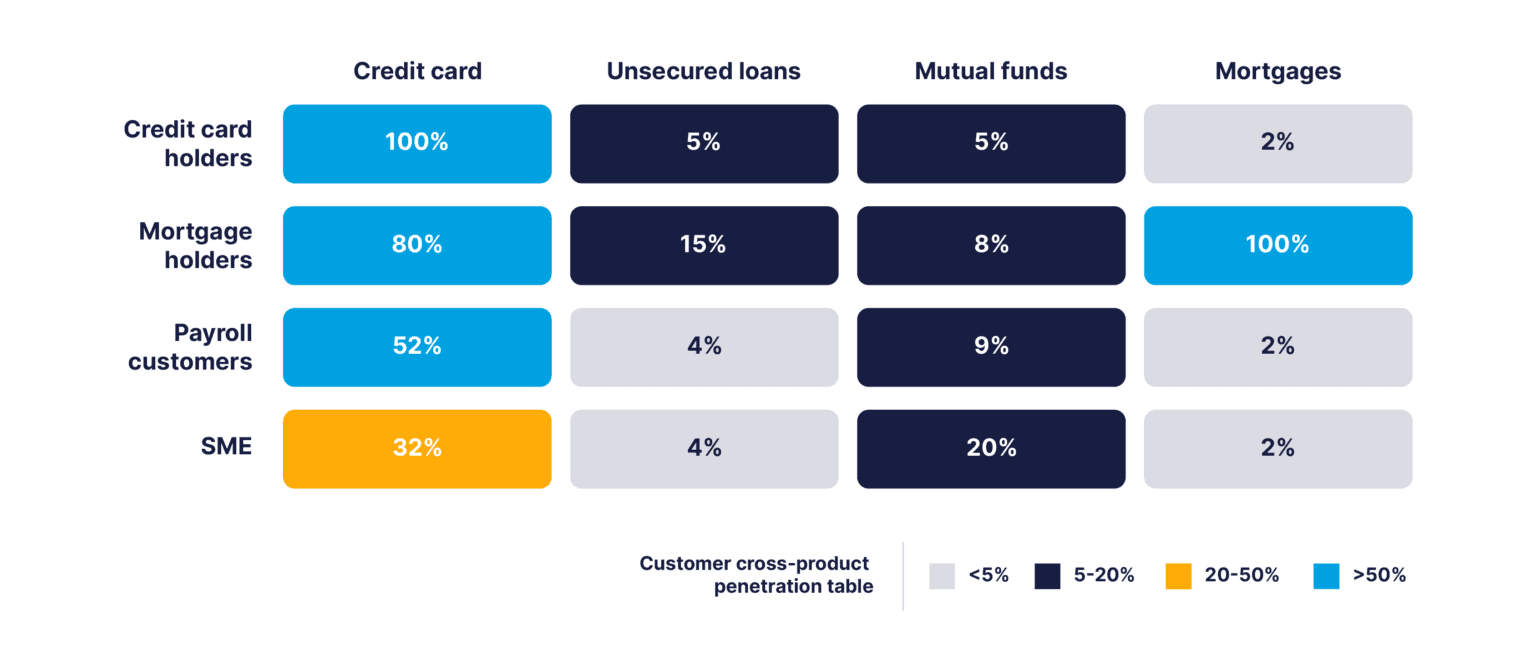

The first step to enhancing your share of wallet is to understand what products your existing customers are using. From a strategy consulting perspective, we will carry out a product penetration analysis. For instance, the team will look at what other products a credit card customer is also using and why that might be.

This is an example of a template that the strategy team often uses, to create a clear picture of where the gaps are in product uptake. For example, the product penetration might find that many of your customers are only using your financial institution for their credit card and savings account but don’t usually apply for a loan. We can then explore the reasons they aren’t and try and find ways to improve the chances that they do.

Understanding customer needs for an increased share of wallet

It may sound cliche, but it’s crucial that you continuously understand the behavior and needs of your customers. By knowing what drives them to bank with you and also what is changing in the world around them can also help improve how many products they hold.

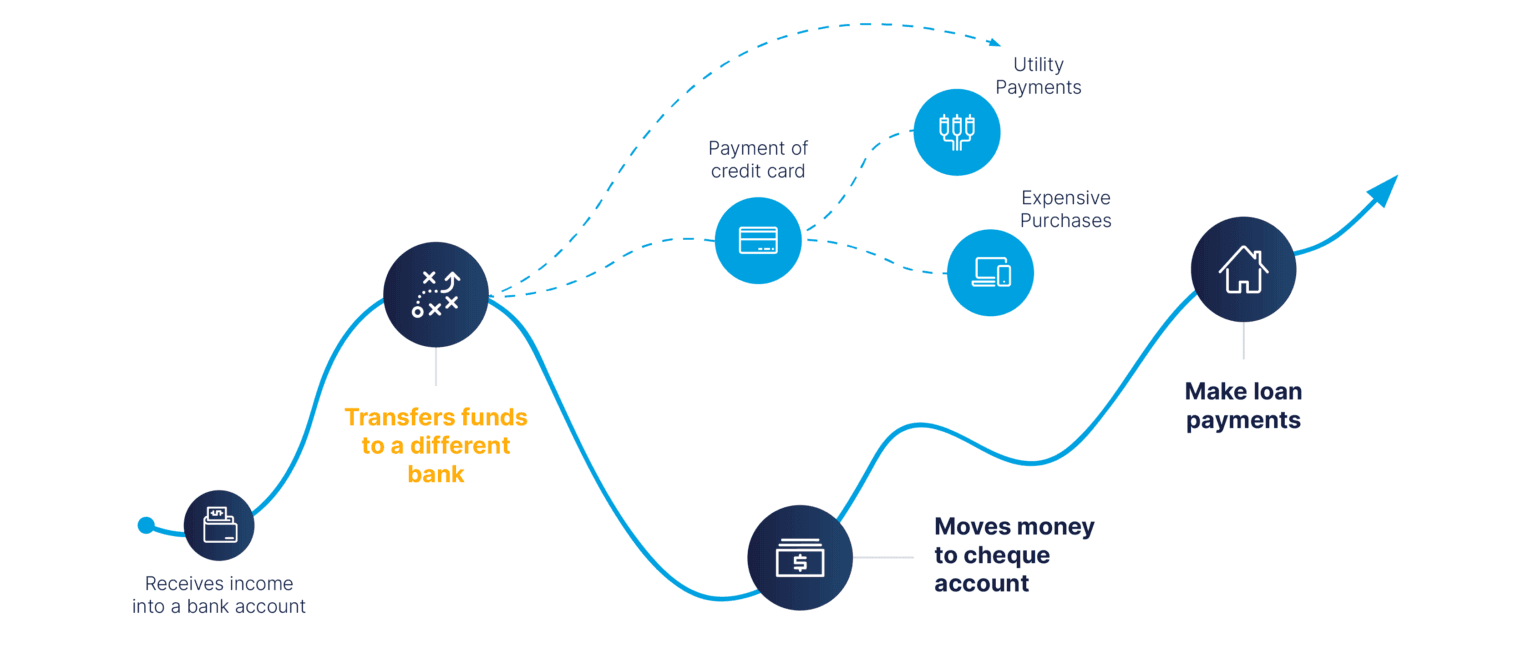

Let’s take the Philippines for example. In order to get a clear picture of their unique behavior and needs, we conducted a series of interviews. It quickly became apparent there was a huge need for loans. During the pandemic, people still had to get into the office for work, but public transportation and ride-sharing services like Uber were not available. So, many people were trying to buy a second-hand vehicle and required a fast way to apply for a loan. Instead of turning to their traditional banks where they might hold a savings account, they would look elsewhere for a speedier and frictionless way to get the loan they needed.

Another insight into Philippine customers was that often they would make purchases with credit cards because most of the time they wanted money left in their savings accounts in case an automatic withdrawal happened.

Implement test campaigns at speed

Once you have this clear understanding of the customers’ wants and needs, then you can target them specifically on your digital platform. For example, you could implement a two-week test with niche customers, marketing an easier loan application process. Once this is completed and the results show at least 30-50% of customers purchased the new product you campaigned then you can take it to all customers.

In order to successfully do test a campaign like this, it’s also vital that you have a platform like the Backbase Engagement Banking Platform that can test and deliver at speed.

Leverage an ecosystem strategy

If a bank is having difficulty in getting customers to purchase more products, they could explore an ecosystem strategy. This is basically leveraging another fintech’s product by orchestrating it on your platform at a cost to them, not the customers.

For example, Revolut’s industry-first move to partner with pension manager PensionBee. This allowed their banking customers to easily manage their pension plans by combining them on one platform.

It’s also crucial that banks are operating on a reliable platform, such as the Backabse Engagement Banking Platform that is able to cope with the speed to market.

By utilizing an ecosystem strategy, banks are able to increase their revenue in a fast way and expand their product offerings to customers. You are also offering additional value to customers by providing them with products or services that go beyond traditional banking.

Overall, there are a string of ways banks can improve their chances of enticing their existing and new customer base to purchase additional products and services. The key to unlocking additional revenue and value for customers is to get to the root of what their unique needs are, as this can change drastically depending on the region and global issues.