How banks are learning fast from other industries

It’s no secret that banks have been blindsided by how much the industry has changed in recent years

by Backbase

It’s no secret that banks have been blindsided by how much their industry has changed in recent years. Their customer base has moved online, learned to consume services via the smartphone, and come to expect the same UX at every touchpoint. Banking in its current form would most likely have been inconceivable a decade ago, yet there it is. In fact, things have changed so much that banks increasingly find themselves looking beyond their own industry for guidance.

This is no surprise, as the best UX experiences are often found in other industries, such as travel or retail. Any bank wanting to compete must have a real understanding of what makes these industries tick, and it’s a journey of discovery that will most likely take them far from home.

New tools for a new world

In many ways, banks have had a lot of catching up to do, and it hasn’t been easy. Bogged down with outdated legacy systems, they have to make UX work via a host of new channels. Customer demands have changed beyond recognition and challenger banks have already moved in to meet those requirements. Consumer demand and modern economics have created pressure to come up with new business models. Consumers expect to have a range of tools at their disposal as they manage their financial lives, many of which the banks simply cannot produce. They must find new ways to keep their client base happy, and that means connecting to those with the right know-how.

Connecting to new technologies will involve much more than collaborating with third parties. It requires a reinvention of the business model. Banks will seek help in negotiating this new territory, and often from the most unlikely partners.

“It’s probably a little out there for banks. But more and more, changing customer expectations and an increasingly digital world are forcing banks to accept the idea of open banking platforms. But they should also bring that thinking to their actual business model.” (Source: Tearsheet – What banks can learn from Amazon.)

Source: Gary Fegan.

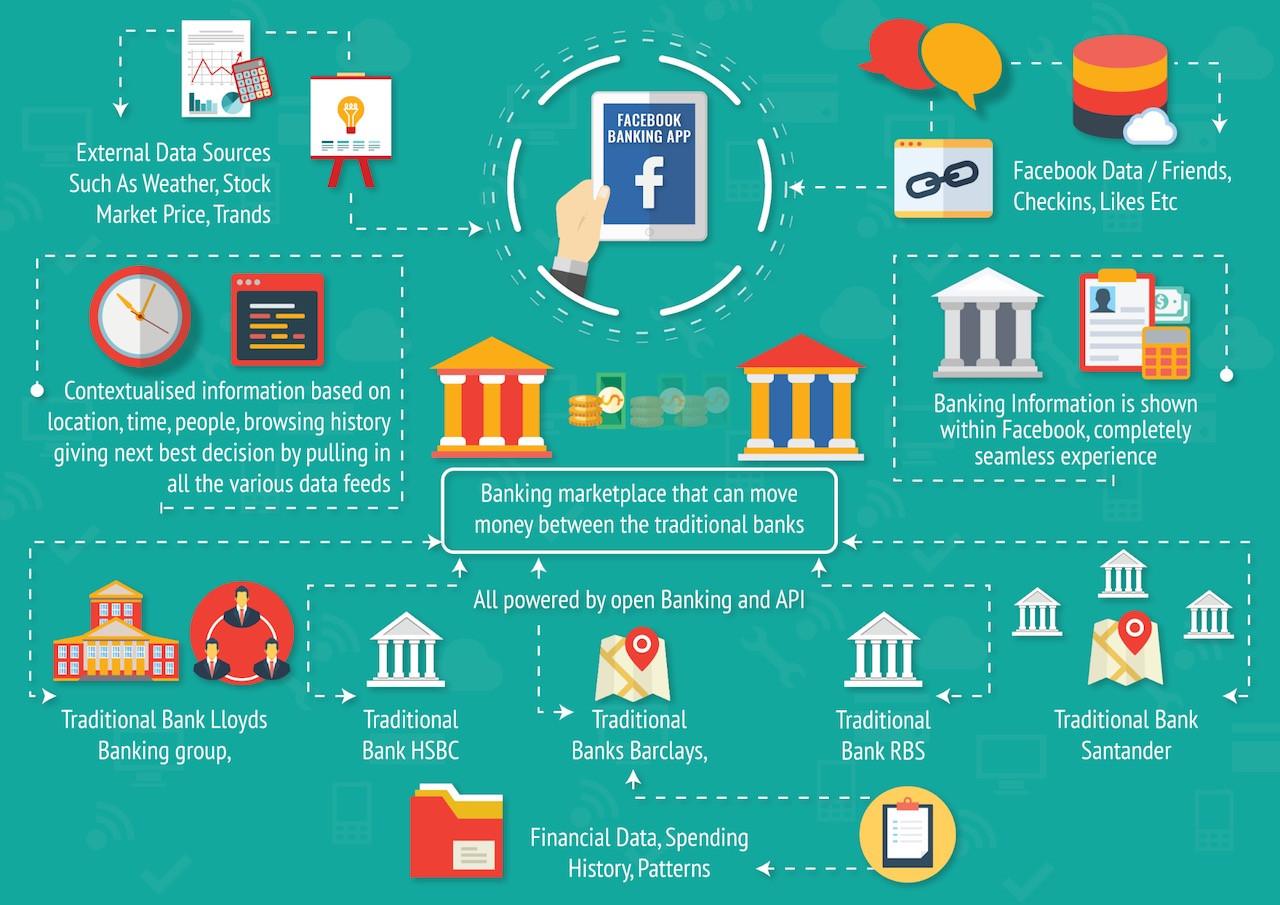

The industry is evolving to the point that “the platformisation of banking” has become a reality. A frightening proposition for many banks, yet also a massive opportunity. By seeing themselves as a platform delivering a range of services, banks have a better chance of tapping into what their customers want, now and in the future.

If operating as a platform is the way to go, then open systems are the foundation of this business model. In this arena, companies such as Amazon, Facebook and Uber have the relevant experience. The secret to their success has been in the proactive approach they take towards open APIs, focusing on the technology’s potential. Financial service companies, primarily concerned with compliance, have honed in less on the upside, leaving them at a relative disadvantage to the likes of Uber, who spurned compliance from the very beginning as they set about disrupting the industry.

Unlikely mentors

With much to learn in a very short space of time, banks need inspiration of an entirely new kind. They must talk to completely unrelated businesses and work with technology partners to get up to speed as quickly as possible. Amazon, Uber and social media channels such as Facebook have blazed a trail in the very areas where banks are seeking knowledge. These open, platform-based providers understand the world today’s customer lives in.

From their very inception, they have operated on that basis, and as a result, have years of expertise that is of real value to banks as they enter the open API economy. Banks need to reinvent themselves to compete, so it’s time to learn from businesses they may have previously considered irrelevant.

Becoming social

Banks can use this newly acquired knowledge to bring their digital transformation to exciting, new levels. A good example of this is the ‘social bank’. A social bank is one that connects to customers via its very own social media ecosystem. It’s a place where social media, wikis, blogs, polls and content sharing are part of everyday business. National Australia Bank (NAB) has become such a bank, providing a range of customer services through social channels. Customer service agents are available on Facebook, Google+ and Twitter. Engagement is also facilitated and enhanced by taking feedback and suggestions through the same channels. Customer involvement is boosted through informative articles, updates and videos, all posted on on YouTube or LinkedIn.

For radical changes such as this, it will be seasoned social media gurus who provide the right direction, not the financial services industry.

In an open API economy, complacency comes with stiff penalties. The old model is simply not an option for banks. Aside from changing how they work, a new outlook is required – one where previous foes become mentors (even partners). It’s a confusing time, fraught with pitfalls, yet a very interesting one. The chance to create the bank of tomorrow has presented itself. Now it’s time to reach out to those who, in some cases, simply know better.