How to build the ideal digital sales solution

To fully leverage the benefits of digital sales, you must put your customers at the heart of your solution. Watch this video to find out how.

by Backbase

In Chapter 3, we explained how financial institutions can fix their digital sales processes—which are broken in most cases and result in more prospects dropping off than converting.

So now you know how and where to begin.

But the next big question is: what should you aim for and why?

So let’s talk about what a modern digital sales solution should look like — and how to bring your vision to life.

Step 1: Conduct UX research to get a deep understanding of your customer

There are three steps you must take to deliver an experience which customers love. The first is putting the user experience (UX) at the heart of the process.

In the last chapter, we explained how silos between the front, middle and back offices are among the most entrenched sources of friction in the financial services industry.

Breaking down these silos is key to enhancing digital sales.

Start with getting everyone in the same room—one team with a common goal.

Your UX designers and researchers should be in the room too. They know what kind of information you need to gather to understand your customers’ requirements. They also take into consideration your back office.

You want to develop a shared understanding and a vision of what you want to offer the end customer.

Ad Terlouw,

Principal UX Designer at Backbase

Next, create a profile of that end customer.

Who are they?

Are they digitally-savvy millennials? Or apprehensive silver surfers?

What are their expectations?

Many have become accustomed to the slick customer experience offered by the latest generation of apps such as Uber.

As a matter of fact, a 2020 study[1] found that when faced with onboarding friction, consumers are walking away in staggering numbers: 63% of consumers have abandoned digital bank applications in the past 12 months –– and one in five of these are due to lengthy processes.

What are they sensitive to?

A report published by the Advertising Research Foundation shows that less than a third of Americans were willing to share their home address with companies in 2019.[2]

How do you think they feel about submitting documents like passports?

Tip: Where are you causing your customers pain?

Figuring out where your customers are experiencing friction on their journey is crucial to improving your digital sales. We listed some of these points in Chapter 1. Here’s just a sample:

Account opening

- How long it takes to complete an application

- The amount of information required

- The delay before customers can access their account

- Limited support

Loan applications

- Customers must provide their own credit score

- The application can’t be completed online

- How long the lender takes to approve a loan

You should also figure out how you rank compared to your competitors. Your Net Promoter Score (NPS) provides a useful benchmark. Your NPS measures the likelihood that a customer would recommend your bank or credit union to a friend. According to Forrester Research, multichannel banks score in the 10-20 range.[3]

Finally, check that your digital sales process meets the regulatory requirements for each territory. For instance, banks operating in the EU must adhere to its Anti Money Laundering Directive. The sixth and latest version came into force at the start of December 2020.

What is the EU’s 6 Anti Money Laundering Directive (6AMLD)?

The EU has introduced several rounds of directives aimed at preventing the use of the European financial system for money laundering or terrorist financing. 6AMLD builds on the previous directives by standardising the definition of money laundering across the EU, expanding the number of offences and extending the liability from individuals to companies.

Bringing the back office into the 21st century

Your support staff will thank you too.

Instead of struggling with user interfaces which are, frankly, stuck in the 1990s, they can focus on developing strong relationships with your customers. After all, the goal of your back office is to provide outstanding customer service.

By overhauling legacy IT systems, you can give your CSR team the optimal tools and processes to do their best work.

Step 2: Test your product to ensure it meets customer expectations

Based on these insights, you can start creating a prototype of your UX. The aim of this step is to design a solution that matches your vision.

Never lose sight of this vision. When customers sign up for an account or apply for products online, it’s your job to ensure the journey meets their expectations.

So what’s the best way to validate your prototype?

Ask your users. Allow your customers to put it to the test. The earlier you get feedback, the easier to incorporate it.

The most important aspect at this stage is understanding that you’re building something your users need. It’s not based on opinion, it’s based on fact.

Caroline van Orsouw,

Product Manager Digital Sales at Backbase

On the other hand, if you wait until the implementation of your digital sales solution is complete, the cost to make adjustments is much higher in terms of time and resources.

Nobody wants to have to break that kind of news to the C-suite.

Step 3: Keep evolving your solution

Never assume that the first version you deliver is the finished product. That’s simply the point at which your customers start to use it. Even if you thoroughly research their requirements before you launch your prototype, you may eventually need to add additional features.

As long as you commit to continuously measuring your progress, the solution you design should meet the constantly changing expectations of your digitally savvy customers.

Essential features for the ideal digital sales solution

When it comes to digital sales, convenience is critical for your customers. In Chapter 1, we pointed out that banks experience a drop off rate of 85% due to a complicated online onboarding process.

How can you stem the flow of customers to the challengers? Make sure your digital sales journey is fast and paperless. That means streamlining the Know Your Customer (KYC) process so your customers don’t have to provide an address history stretching back several years. That means digitally verifying ID so they don’t have to visit a branch (especially amid a pandemic). And that means offering the option to complete the application on any device.

Here’s some more food for thought.

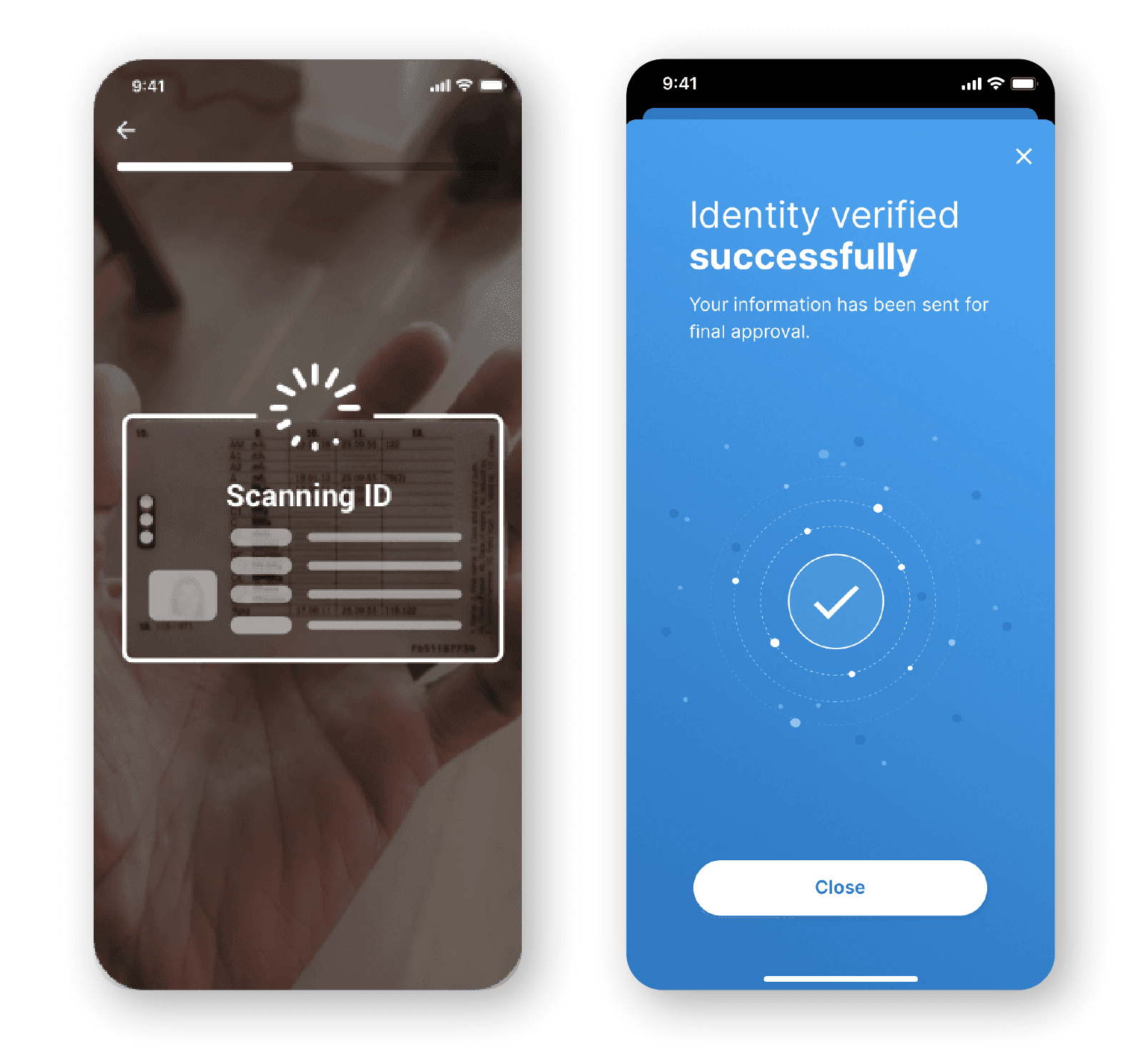

eIDV (Electronic identity verification)

Verifying your customer’s identity is an important step in meeting your KYC requirements, but you shouldn’t require them to visit a branch just for that purpose. And here’s a good reason why: 32% of customers refuse to even start an application if they are required to take ID credentials to a branch. [4]

Making sure that your digital account opening solution integrates eIDV will make a huge difference. All your customers need to do to verify their identity is to simply scan their passport, and they’re good to go.

Above: Instant identity verification with Backbase Digital Sales

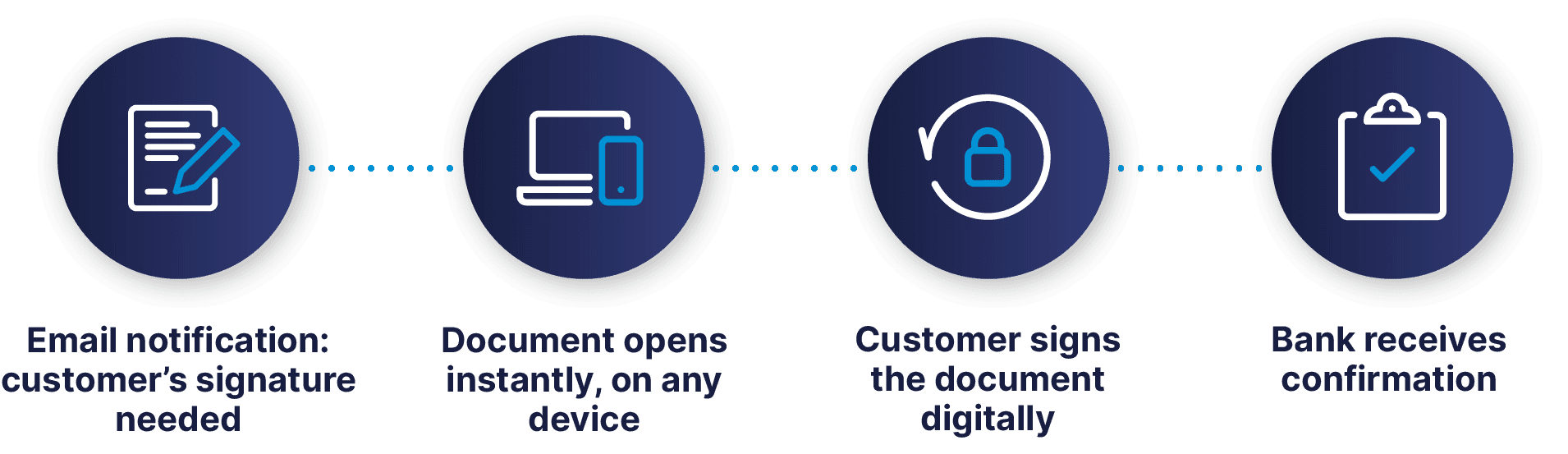

E-signatures

E-signatures allow customers to digitally sign a document instantly, on a device of their choice, from the comfort of their own home. DocuSign, a widely used e-signature platform, estimates that providers can save $36 per document, while over 80% are signed within 24 hours.

How e-signing works

Application center

In Chapter 3, we critiqued how banks often go silent once onboarding is complete. Customers are left wondering about the status of their application and when they may get access to their account or funds. Just ask anyone who has applied for a mortgage how that feels.

However, banks and credit unions provide much greater transparency if they incorporate an application centre into the onboarding or product origination process. Customers can log into the centre and keep track of their application’s progress through the system.

In case of delays, for example if an employee needs to make a manual intervention, the customer receives an update explaining why. Providing this level of reassurance prevents customers from abandoning the process and beginning it again with one of your competitors.

It’s time to revitalize your digital sales processes

By following these steps, you give your bank or credit union the best chance of leveraging the considerable benefits digital sales offers your customers and boosting your bottom line.

You also design a solution which is reusable and scalable, and one which delivers an unrivalled experience for your customers, not to mention your employees.

Here at Backbase, we practice what we preach.

We work closely with our clients to deliver a high-quality digital sales solution which works across every business line in retail banking, SME banking and wealth management. And it goes without saying: our solutions work on all channels and devices. Whether you need a bespoke solution, or require some out-of-the-box digital sales firepower that you can implement and scale quickly across your product lines, we can help.

In the next chapter, we'll demonstrate how a retail bank can offer their customers an oustandingly convenient digital onboarding and financing experience.

Read on: [Demo] The modern retail bank's digital onboarding and lending process