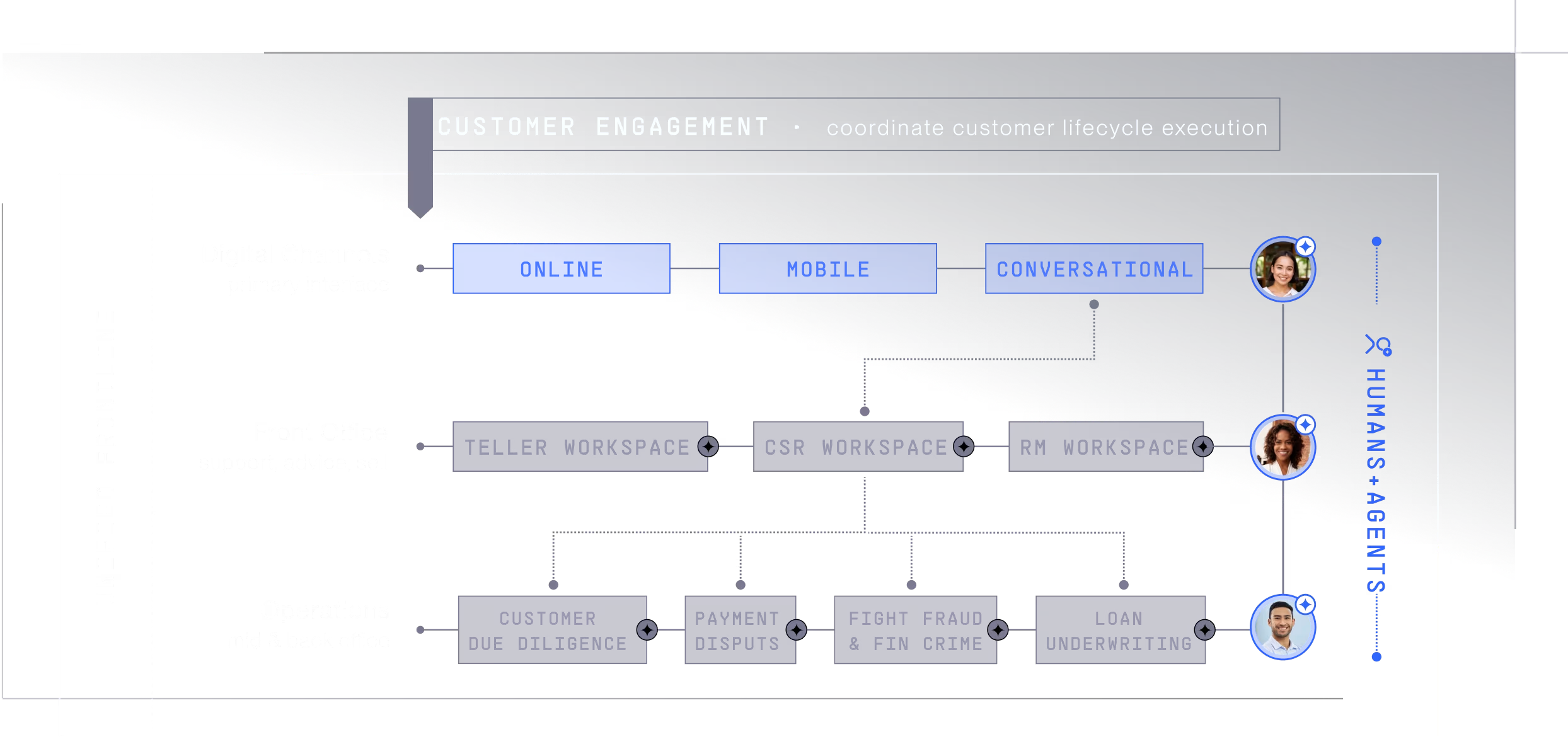

.svg)

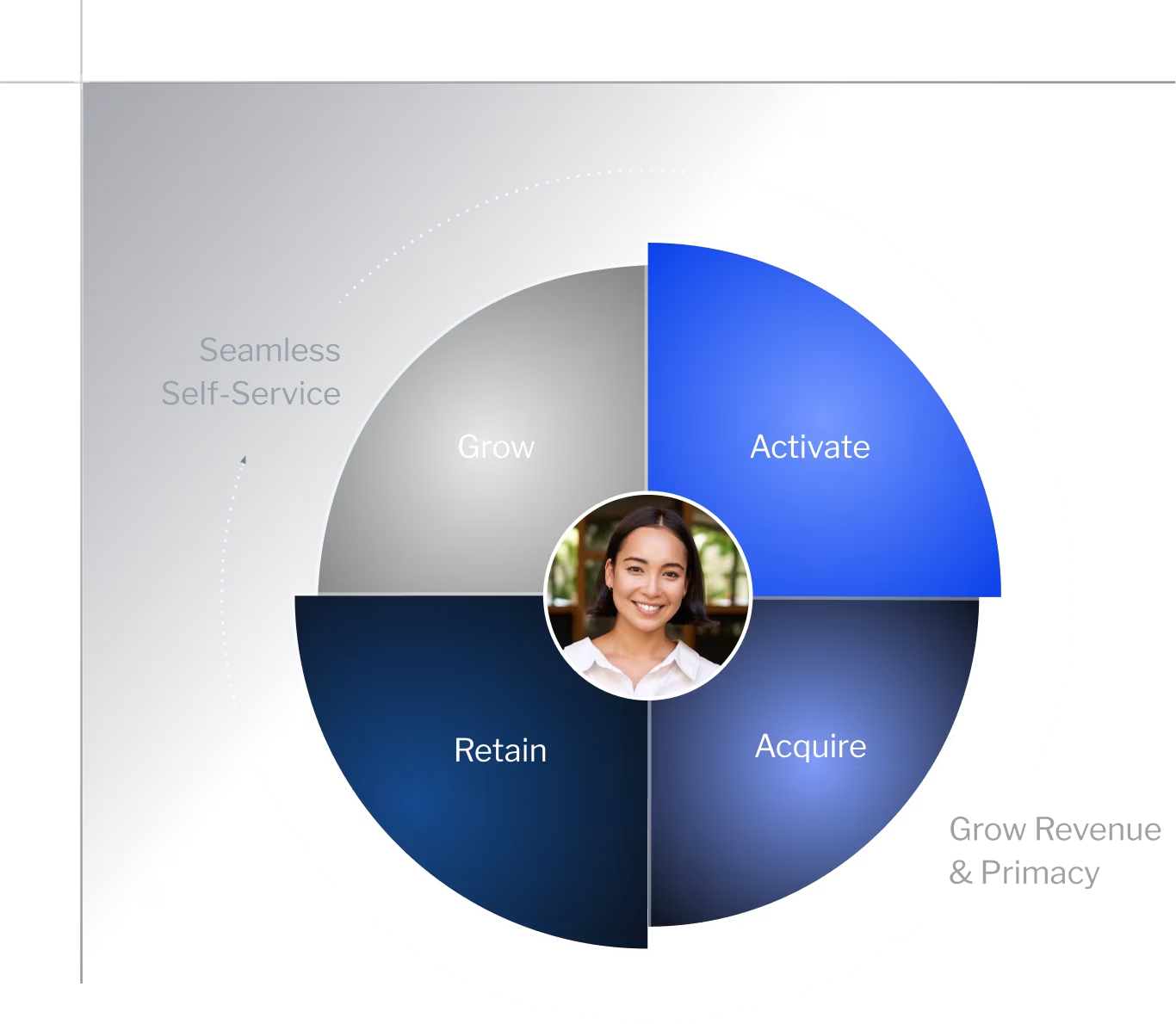

Self-service first.

Humans and agents on demand.

Online, mobile, conversational - the customer is in control, on shared context across every channel. Employees step in when judgment matters. Agents step in when speed does. The Banking OS orchestrates the lifecycle so every interaction picks up where the last one left off.