Creating harmony between business and customer value

Australian and New Zealand banks face a brutal reality: digital transformation has destroyed traditional competitive boundaries while customer expectations have skyrocketed. Legacy technology is the anchor dragging banks down when they need to move fastest. The banks winning today have cracked the code on balancing operational efficiency with exceptional customer experience.

The 'banking fly-wheel effect'

The banking flywheel effect is the self-reinforcing cycle where customer value and business value feed each other to create unstoppable momentum. When banks nail both sides - operational efficiency and customer experience - they trigger exponential growth that competitors can't match.

Australian and New Zealand banks are burning tens of millions on core banking transformations. These projects fix the back-end but ignore what customers actually see and feel.

The Core Banking Blind Spot

- Back-end focus: Banks upgrade systems for operational efficiency and risk management

- Front-end neglect: Customer-facing experiences remain clunky and disconnected

- Wasted investment: Millions spent without improving customer satisfaction

In today's convenience-driven world, where digital engagement and user experience are paramount, it's essential for banks to complement their core system upgrades with modern, flexible digital channels.

Customers expect intuitive, real-time services through web, mobile, and other digital interfaces. Without robust and agile digital solutions, even the most efficient back-end processes may fall short of delivering the customer-centric experience that is becoming the competitive differentiator for banks. Both internal efficiencies and customer-facing innovation need to evolve in tandem to meet the expectations of today's consumers.

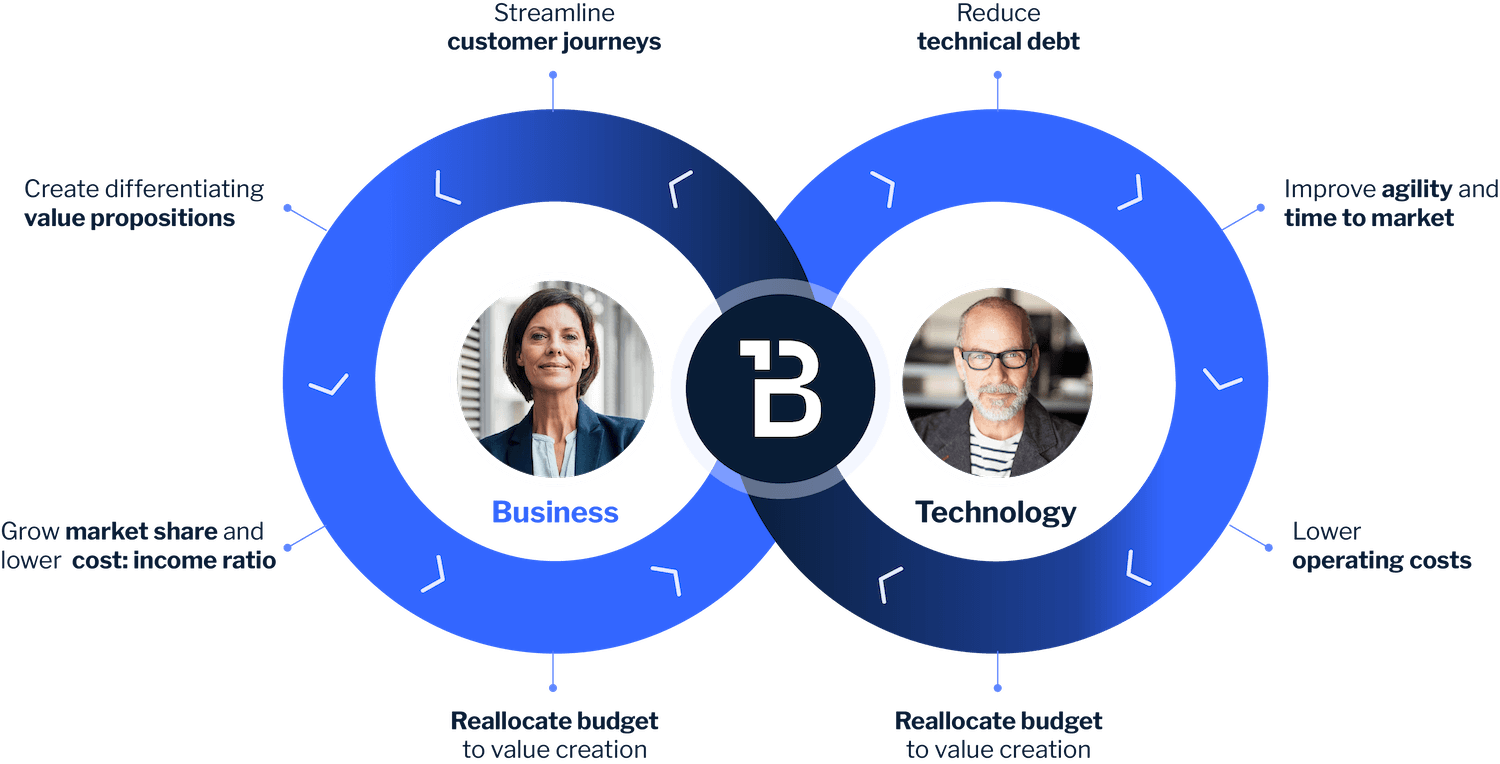

The two sides of the fly-wheel

The banking flywheel has two sides that must spin together. Customer value drives business value, which funds better customer value - creating unstoppable momentum.

The banking flywheel consists of two primary components:

- Customer value: This side of the flywheel represents the bank's ability to deliver value to its customers. It encompasses factors such as customer satisfaction, loyalty, and advocacy. By investing in customer experience initiatives, banks can enhance their customer relationships and drive revenue growth.

- Business value: This side of the flywheel represents the bank's financial performance and profitability. It includes factors such as revenue growth, cost efficiency, and market share. By optimising operations and leveraging technology, banks can improve their bottom line and strengthen their competitive position.

The power of synergy

While both sides of the banking flywheel are important, their true power lies in their synergy. When the customer value and business value sides work together, they create a self-reinforcing cycle that can drive significant momentum.

By investing in customer experience initiatives, banks can increase customer satisfaction and loyalty, leading to higher revenue and market share. This increased revenue can then be reinvested in technology and other initiatives to further enhance the customer experience, creating a virtuous cycle.

How the Flywheel Works

- Customer satisfaction increases: Happy customers stay longer and buy more

- Revenue grows: More profit funds technology and experience improvements

- Operations improve: Better systems create even better customer experiences

Harmonizing the flywheel

To effectively harmonize the customer value and business value sides of the banking flywheel, banks should consider the following strategies:

- Invest in technology: Technology plays a crucial role in driving efficiency, improving customer experiences, and enabling innovation. By investing in modern technology solutions, banks can streamline processes, reduce costs, and offer personalized services. This includes areas such as digital banking, artificial intelligence, and data analytics.

- Prioritize customer experience: Customers are at the heart of the banking flywheel. Banks must focus on delivering exceptional customer experiences by understanding their needs, preferences, and pain points. This can be achieved through personalized interactions, convenient channels, and proactive support. For example, banks can leverage data analytics to identify customer preferences and tailor their offerings accordingly.

- Optimize operations: Efficient operations are essential for maximizing profitability. Banks should continuously review and optimize their processes to identify areas for improvement. This may involve automation, streamlining workflows, and reducing costs. For instance, banks can use robotic process automation (RPA) to automate repetitive tasks and improve efficiency.

- Foster a culture of innovation: Innovation is key to staying ahead of the competition and meeting the evolving needs of customers. Banks should create a culture that encourages experimentation, creativity, and a willingness to embrace new ideas. This can be achieved through initiatives such as hackathons, innovation labs, and employee training programs.

- Measure and analyze performance: To track the effectiveness of the banking flywheel, banks should establish key performance indicators (KPIs) and regularly measure their progress. This data can be used to identify areas for improvement and make informed decisions. For example, banks can track metrics such as customer satisfaction, net promoter score (NPS), and return on investment (ROI).

Overcoming challenges

Banking Flywheel Challenges

What stops banks from building flywheel momentum?

Legacy technology creates friction that breaks the flywheel cycle. When systems can't talk to each other, customer experience suffers and operational costs soar.

How do data privacy regulations impact the flywheel?

Strict compliance requirements can slow innovation, but banks that build privacy into their flywheel strategy gain customer trust and competitive advantage.

Why do customer expectations keep breaking the flywheel?

Customer expectations evolve faster than bank technology can adapt. The flywheel only works when banks can pivot quickly to meet new demands.

To overcome these challenges, banks must invest in modernization initiatives, implement robust data security measures, and continuously monitor and adapt to changing customer needs.

Creating a sustainable path to growth and success

Banks that master the flywheel effect don't just survive - they dominate. The momentum they build becomes their competitive moat.

Flywheel Success Metrics

- Revenue acceleration: Customer lifetime value increases 25-40%

- Cost reduction: Operational efficiency gains of 15-30%

- Market position: Customer acquisition costs drop while retention soars

The banking flywheel isn't theory - it's the difference between banks that lead and banks that disappear.