Middle East banking just posted one of its strongest quarters on record.

In the UAE, six major banks delivered ~Dh26B+ in combined net profit. FAB crossed $400B in assets, ADCB was up 30-37% YoY, and Mashreq grew operating income to AED 3.4 billion, with customer loans expanding 33% year-on-year.

In Saudi Arabia, the Kingdom's ten listed banks posted a record $6.4 billion in combined Q1 profit, up 7.6% year-on-year, driven by credit demand tied to Vision 2030 and expanding retail and mortgage lending.

Across the GCC, Moody's upgraded its outlook for the UAE banking sector from stable to positive in February 2026, citing resilient non-oil momentum and improving credit conditions.

The picture across markets, segments and balance sheet lines points consistently towards broad-based strength. Yet, in most of my conversations with banking leaders across the region, the question I keep hearing isn't about the results. It's about what comes next.

How do you sustain growth without complexity growing with it? How do you scale without adding proportional headcount? How do you make AI actually work, not just in a pilot, but across the bank?

These aren't new questions, but they're more urgent than they've ever been.

How we got here: the architecture problem AI exposed

Every generation of banking technology solved one problem and left a harder one behind.

- 2005-2015 · Digital banking apps gave banks digital channels. Customers could check balances, transfer money and pay bills without visiting a branch. It worked, but the bank behind the window didn't change. The customer experience got better, but the cost structure didn't. Employees still toggled between disconnected systems and operations still ran on manual coordination.

- 2015-2024 · Engagement platforms unified the customer journey. Onboarding, engagement and lifecycle management came together on one platform. Banks like those posting strong results today built real momentum here, doubling onboarding rates, growing digital adoption and creating consistent experiences across touchpoints. But the work underneath, such as KYC reviews, lending decisions, dispute resolution and customer servicing, still depended on people filling the gaps between systems manually.

- 2025 · AI-powered banking brought AI into the picture, such as chatbots, fraud models, document processing and recommendation engines. While this brought real value in specific domains, AI deployed on a fragmented foundation doesn't compound. It creates a more expensive version of the same problem, whereby every model runs on partial data and every deployment starts from scratch. Banks were investing in intelligence without the architecture to sustain it.

This more expensive problem is called the operational whitespace. 50% of frontline banking work doesn't live in any single system, but between them. It manifests in the handoffs, the exceptions and the manual coordination. It is why employees sometimes need to open six screens to answer one customer question - sometimes even copy-pasting between sheets and systems.

That's where operational cost lives, and until now, no generation of banking technology has solved it.

A new actor changes everything

There's another reason this moment is different from every previous cycle.

For 20 years, banking ran on two actors: The initiating customer and the executing employee. Every system, process and approval chain was designed around that interaction.

A third actor just joined the floor: The AI agent.

The AI agent neither waits to be asked nor works off a screen. It reads context, makes decisions and triggers actions in seconds, across systems, without a human in the loop. Unlike every previous technology wave, it doesn't just change how work gets done, but changes who does it.

💡 Pro tip: Those still operating with only two actors will increasingly feel the gap in agility, cost efficiency, and in delivering the level of service customers now expect.

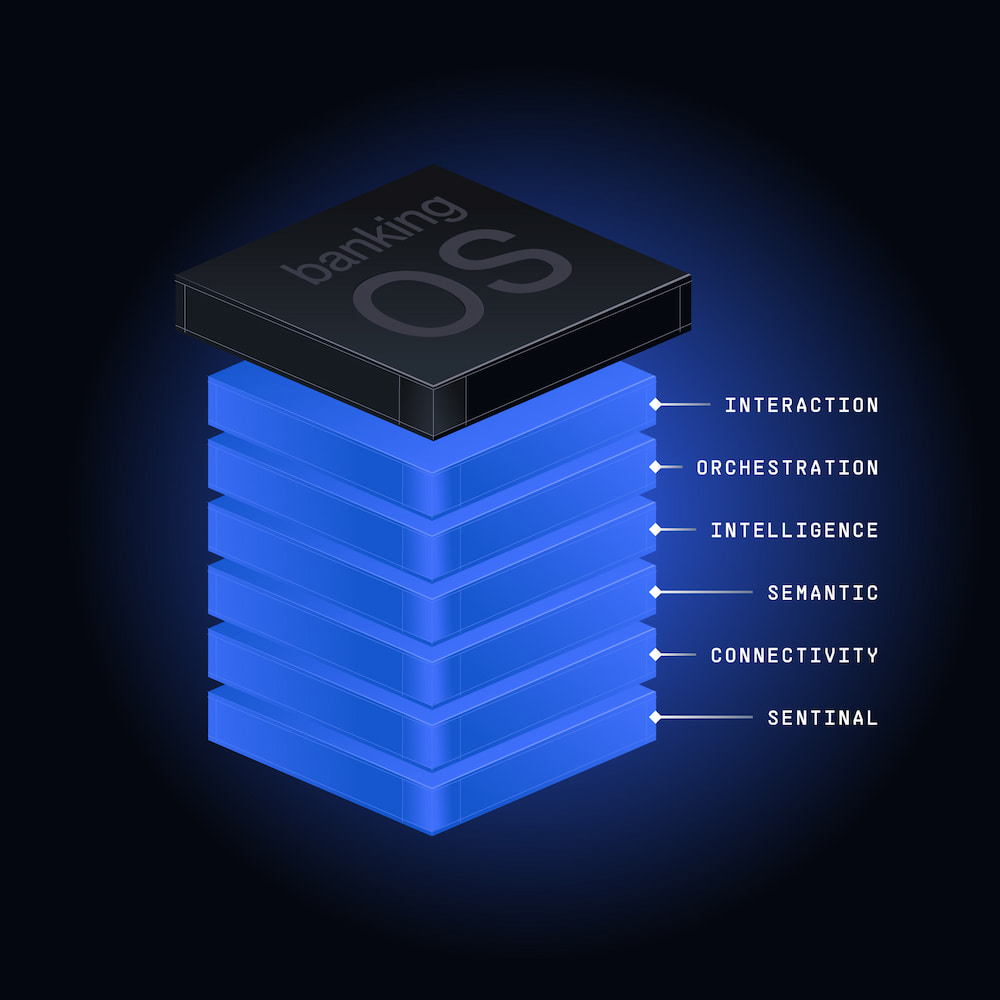

What the next operating model for banks looks like in 2026

2026-present · AI-native Banking OS. At Backbase, we believe this development represents the next architectural generation of banking technology. This time, the goal isn't another capability layer. It's closing the gap that every previous generation left open.

This does not mean that we are revealing another channel or adding AI on top of current operations. Instead, this refers to an operating layer that sits above your existing infrastructure (core banking, CRM, payments, cards, etc.) and coordinates the work between them in real time.

One important clarification for banks that have invested in their own platforms: the Banking OS doesn't compete with what you've built. It sits above it. Whether your bank runs a proprietary in-house stack or a major core, the operating layer connects above those systems, not through them. That's the coexistence model, and it's how Tier-1 banks across the region are approaching it.

The outcome is what we call Elastic Operations: the ability to scale throughput without scaling headcount linearly. Agents absorb routine work, while employees focus on what requires human judgment. Every decision is traceable and every action is authorized. The whole system gets smarter with every interaction because intelligence is built into the foundation, not layered on top of it.

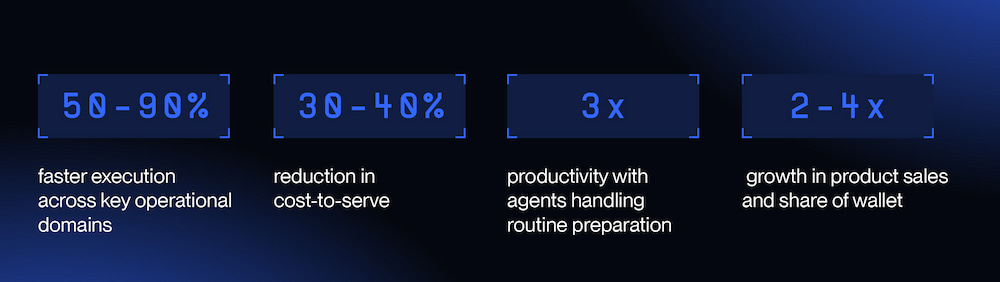

Banks that have completed this kind of operational transformation are reporting measurable results across three areas:

- 2-4x growth in product sales and share of wallet

- 50-90% faster execution across key operational domains

- 30-40% reduction in cost-to-serve

- 3x staff productivity with agents handling routine preparation

These aren't incremental improvements, but the result of fixing the operating model and architecture underneath.

Why this moment matters, especially in the Middle East

The Q1 numbers across the Middle East are a signal that two forces are currently converging to make the shift from platform to operating system unavoidable:

Force 1. Your customer base shifted while your cost base didn't.

Across the Gulf, the customer your bank is trying to win is younger than most banks were built for. KSA's median age sits under 30. The UAE and Qatar run 80%+ expat populations with global service expectations. The cost base most banks still operate on was built for a different generation: branches, call centres, and manual underwriting.

The structural answer isn't a better mobile app on a legacy stack. It's a different operating model. Banks that get this right serve digital-natives at a fraction of the cost-to-serve and reinvest the margin into depth. The ones that don't keep losing share at every channel they don't own.

For Tier-1 banks like FAB, ENBD, and QNB, this is not a neobank story. Neobanks show where customer expectations have moved. They do not show the path forward for a $400B universal bank.

The Tier-1 advantage is scale - but only when the operating model can use it. A bank that can coordinate customers, employees, and AI agents across one unified frontline will outperform any challenger on efficiency, control, and depth of relationship. That cannot be replicated from scratch.

Force 2. AI is already in your bank, but the question is whether it's coordinated.

Banks across the GCC are deploying agents across fraud, servicing, onboarding, underwriting and compliance. Without a coordination layer, every new AI agent makes the problem worse. Each one runs on incomplete data, follows its own rules, and has no shared context with the rest of the operation. More agents means more fragmentation, not more capacity.

Regulators across the region are moving toward a clear standard: every decision, whether made by a person or an AI agent, must be traceable and provable. That cannot be added on top of individual models after the fact. It has to be built into how the system works.

2030 isn't the question. 2026 is.

The banks that build the right operating model this year, with the architecture to support it, are the ones competitors stop trying to catch by 2027.

If your bank is working through that architecture decision, it's worth comparing notes on what we're seeing across the region.