Introduction

Just like every other financial institution in the world, your bank is probably already brainstorming the best ways to leverage Artificial Intelligence (AI). Whether you’re interested in using this cutting-edge tech to boost efficiency, better engage your customers, or provide them with personalized financial recommendations, we’re all racing the clock to be one of the first to meaningfully adopt it — and become customers’ primary banking relationship.

Unfortunately, adopting AI isn’t as easy as flicking a switch. In fact, there’s three common barriers that are holding banks back from making the most of this tech. Let’s take a look.

1. Making the paradigm shift

Bear with us here, this one is the most obvious, but it’s also incredibly important. Many banks are still looking at AI as a futuristic product, rather than something they can actually use now, in their day-to-day operations. Because AI is sufficiently advanced, traditional banks in particular have incorrectly assumed it’s the solution to tomorrow’s problems, not today’s. How, they reason, can we adopt this technology if we’re still struggling to deal with our legacy systems, point solutions, and operational silos? We’ll get to all of that soon, but it’s key to understand that, while AI is ground-breaking tech, its usage is eminently achievable and any bank can leverage it — provided they build a solid foundation in advance.

But the first step is making the paradigm shift and seeing AI for what it is: just another tool, albeit an advanced one. Remember this is far from new tech. While we’ve come closer to “perfecting” various exciting use cases in recent years, we can see early examples of AI in financial services back in the 1990s, when banks were already able to use it for rudimentary investment, debt, and retirement planning, budget recommendations, and more. It’s not space-age technology, and your bank can absolutely find a way to make use of it. You’ll just have to put in some legwork first.

2. Determining your business case

Before you can even think about adopting AI, your bank will need to determine the specific business case you’d like to use it for. Just ask Chris Shayan, our Head of AI.

“Always start with the business case so you can actually define what’s needed to get it done,” Chris explained, in a recent interview. “Ask yourself why you want to adopt AI; what’s the problem you want to solve? If you scope down the business case, then automatically, you're scoping down the risk and cost as well, and then we can have a proper conversation about ROI.”

We’ve already seen banks start to rush AI value props to market, but this will never work unless you have a clear vision for its usage. Otherwise, you’re just throwing money into your tech stack, and that’s a recipe for disaster.

Did you know that

64% of CEOs say they’re happy to invest in new tech, even without a clear ROI, just to keep pace, according to a recent survey — a strategy that will never yield long-term success.

So whether you want to use it for business applications — like process automation and fraud detection/prevention — or customer applications — like personalized financial advice or customer support — you need to determine your business case up front. But to get the most out of AI — as well as the underlying data that powers it — you’ll need to harness the power of a platform model.

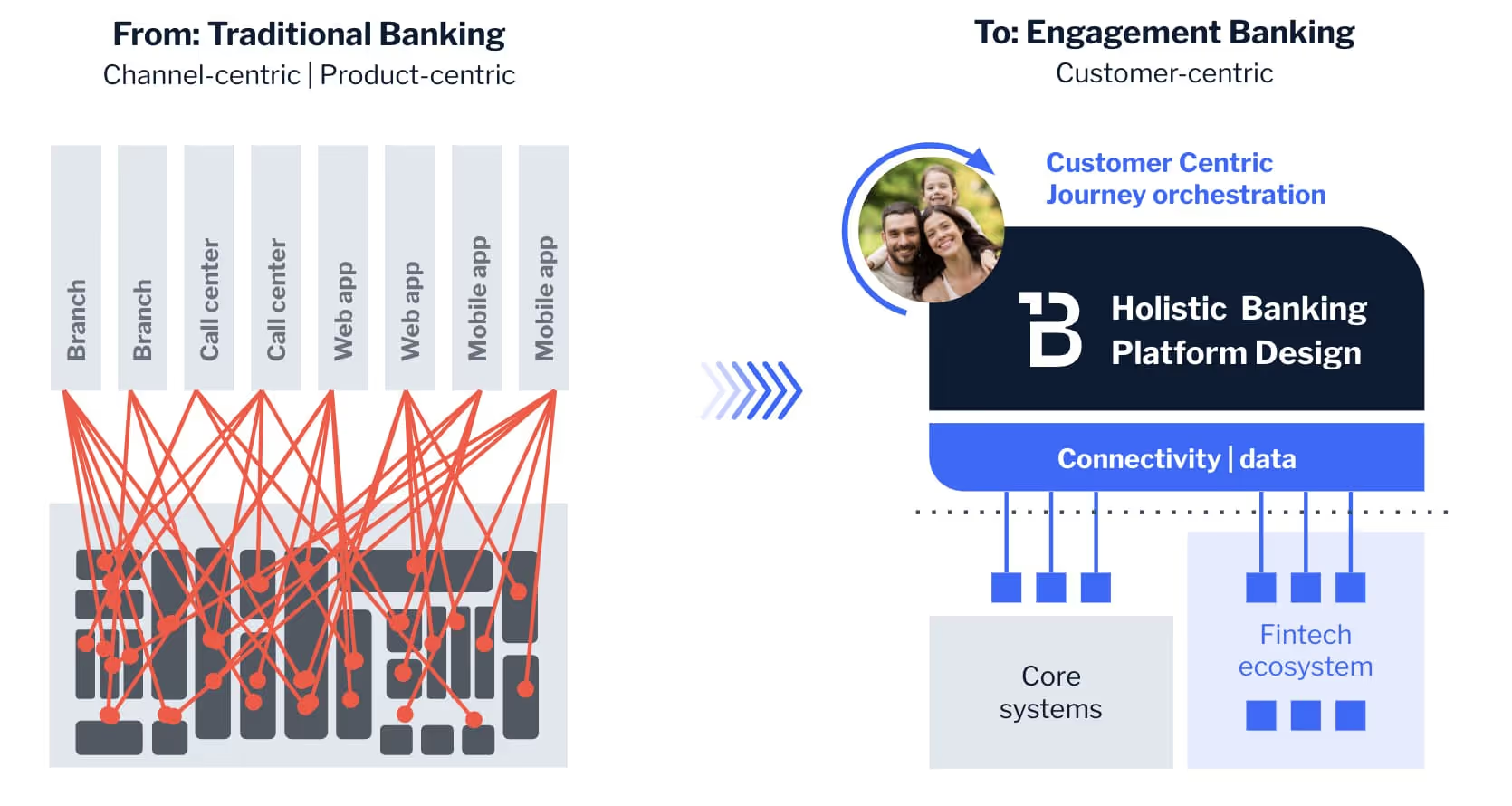

3. Adopting a platform model

While your legacy systems are perfectly able to leverage the kind of AI that was developed in the 90s, modern AI — and its associated use cases — are a different matter. To effectively use AI today, your bank will need to first adopt a cloud-native, microservices-driven platform that makes experience orchestration easy.

Chris spoke about this in episode 25 of our Banking Reinvented podcast:

“AI can be easily managed by existing technologies, but you need to have a platform for your customer experience orchestration, one that’s fully microservice-driven,” he said. “Then, it’s a very natural move.”

The alternative is building everything from scratch, but that’s enormously time-consuming and costly, and your bank simply doesn’t have that luxury, not with the clock ticking.

Of course, adopting a platform model can seem like a massive leap if you’re coming from decades-old, siloed tech. But it’s easier than it sounds. By taking a progressive approach to banking modernization, you’ll be able to minimize cost, time, and risk as you gradually upgrade your bank’s infrastructure, technology, and processes. It all starts by upgrading things, journey by journey, prioritizing high-impact, customer-facing areas that will immediately demonstrate value. Once you’re ready, you can gradually roll out and then move on. It’s a strategy that allows you to accelerate delivery, reduce complexity and anchor your bank’s priorities firmly in the customer experience.

Taking the first step

We won’t sit here and tell you that AI in banking is easy to adopt. It isn’t. But it is significantly easier than your bank may fear, particularly when you make the paradigm shift, plan out your business case, and harness the power of a single, unified platform. So start planning today, and remember that time is of the essence. As banks continue to hop on the AI bandwagon, it will become harder and harder for you to catch up. Take it from Chris:

“When microservices became popular, I told my team that it was a ‘reset moment,’” he said. “If we didn’t adapt, it would just be a matter of time before we couldn’t go to the next level, and I think it’s the same with AI, especially with the new capabilities of LLMs. Banks need to evolve quickly if they want to keep up.”

For more information, check out our Banking Reinvented podcast, where host Tim Rutten dissects similar topics alongside other digital leaders. Stay tuned as they chat about everything from progressive modernization to decomposing your bank’s complexity.