Introduction

For decades, private banking has thrived on the trust and personal connection between relationship managers and their clients. The RM is the trusted advisor to the client, guiding them through everything from wealth structuring to family legacies and strategic investments.

But the world around private banking has shifted dramatically. New generations of wealth holders are more digital-savvy, and more demanding. Self-made wealth creators are rewriting the rulebook. Compliance pressures are rising. And all of this is happening while banks face stubbornly high cost-income ratios and fixed operational models that limit flexibility. Expectations are changing, and clients want digital sophistication and personal service — not one or the other.

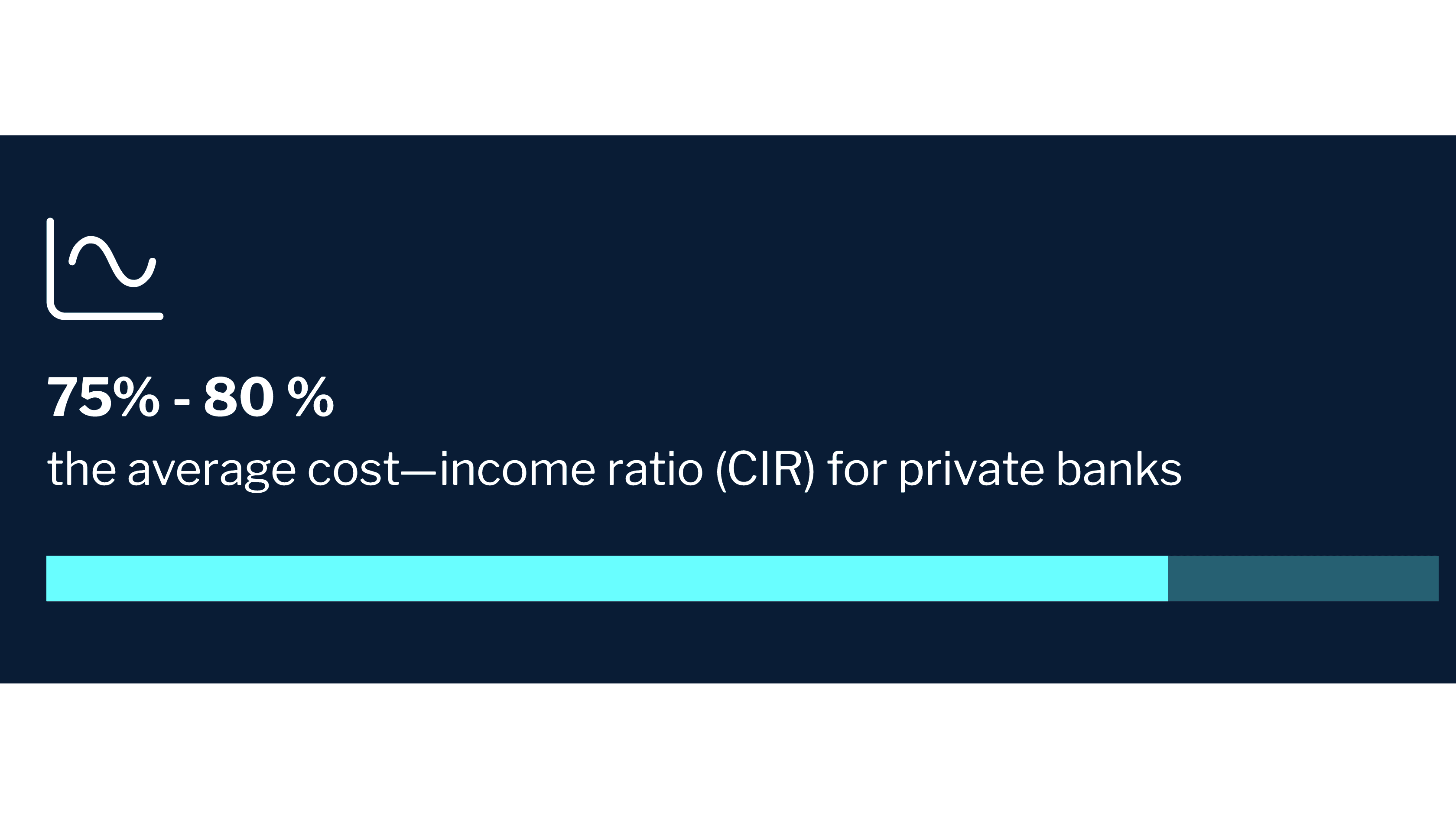

Cost-income ratios often sit between 75% and 85% according to Deloitte, with more than half of costs locked in as fixed. Relationship managers, the very heart of private banking, are often bogged down by admin. As McKinsey notes, some spend up to 70% of their time on non-client tasks. This not only creates a significant barrier to growth but also undermines the client experience, leading to dissatisfaction and lower NPS.

The evolving role of the relationship manager

Many HNW and UHNW clients today are digital-first, expect instant access to information, and want a service model that matches the convenience of consumer tech and luxury brands. Whether they’re entrepreneurs, creatives, or heirs to family wealth, they won’t tolerate clunky onboarding or outdated advice delivery; according to EY, nearly 60% of Millennials favor wealth managers who proactively enhance their digital platforms, compared to just 40% of the broader client base.

Private banking is moving toward more structured, value-driven models, with advisory and discretionary mandates becoming the norm, especially as client assets grow.. No longer is it enough to simply execute trades — clients now expect tailored advice that anticipates their needs.

Beyond service, this shift is also about strategy; these mandates provide a foundation for deeper engagement and help justify higher fees through demonstrated value. Relationship managers are expected to offer proposals that align with client goals, but doing this effectively at scale remains difficult. Here’s why:

What’s holding relationship managers back

Despite technology investments, many private banks remain hamstrung by operational inefficiencies. RMs often work within disjointed environments, toggling between legacy CRMs, manual document processing, and siloed data sources.

The compliance burden also continues to mount. Know Your Customer (KYC) processes, Anti-Money Laundering (AML) checks, and onboarding documentation have grown in complexity and length. Onboarding a UHNW client, particularly one involving family trusts or cross-border holdings, can still require weeks of back-and-forth, paper trails, and internal approvals.

This stands in stark contrast to the world these clients are used to. In their everyday lives, they expect instant gratification: same-day bespoke car deliveries, last-minute luxury travel, or 24/7 lifestyle concierge services. They live in an ecosystem of immediacy, so when a bank takes weeks of paperwork to complete a process, the experience feels completely out of sync.

In comparison, fintechs offer onboarding experiences that take minutes, not weeks. While they aren't direct competitors to private banks, they are significantly reshaping expectations — particularly around speed, convenience, and mobile-first interaction.

Efforts to improve RM productivity through digital tools often fall short because they fail to address the end-to-end nature of the relationship manager’s role. Tools that automate isolated tasks do not go far enough in transforming the full client journey and freeing up RMs to focus on client meetings and revenue-generating activities.

How to redesign RM workflows for impact

To drive growth in a demanding landscape, private banks must enable relationship managers to spend less time navigating systems, and more time doing what truly matters: building relationships, strengthening client trust, reducing churn, and deepening wallet share across generations. That requires a step-change in how productivity is defined and delivered.

1. Performance backed by data

When RMs are equipped to perform at their best, the impact on the business is substantial. McKinsey research shows that private banks in the top quartile for RM productivity saw assets under management (AuM) grow 12% annually, more than double the industry average. Their profits outpaced peers by three percentage points each year.

And when the solution is to try to grow just by adding more RMs without making them more productive, the results are less satisfying. The banks that only tried increasing the number of RMs actually saw profits shrink by 3% per year.

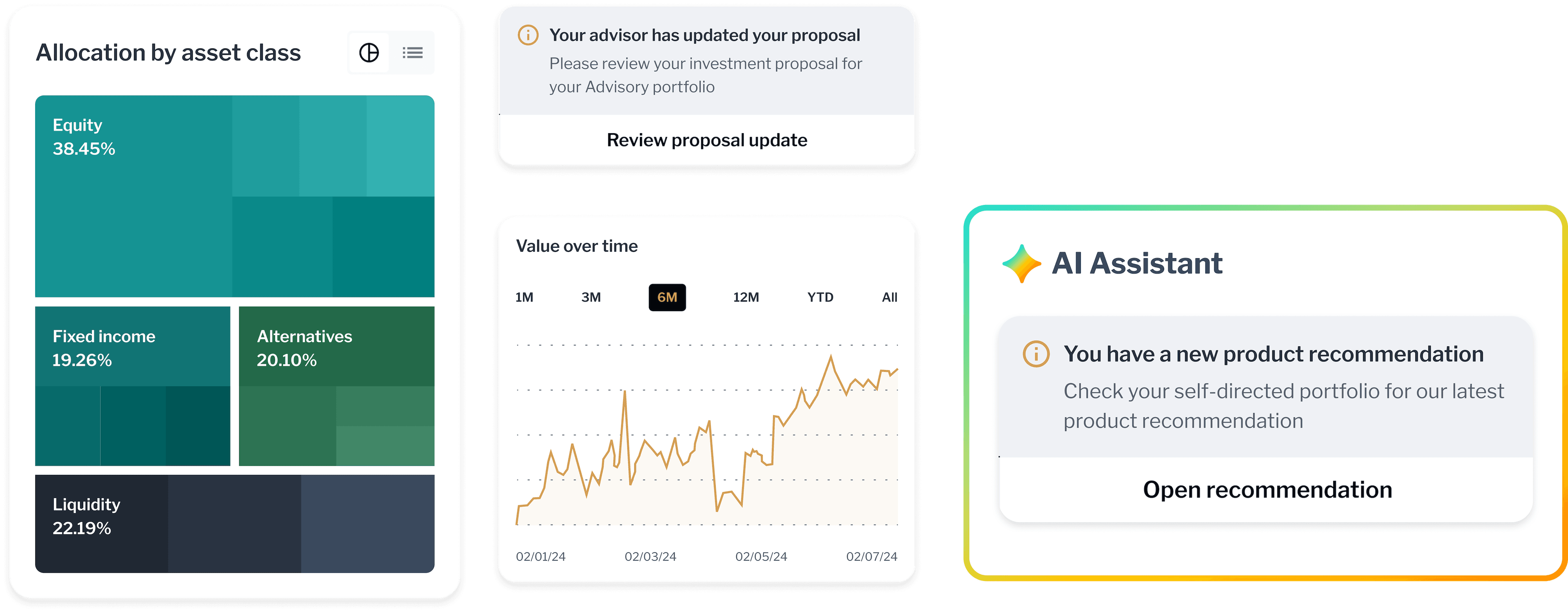

2. Unified workspaces for better collaboration

Instead of toggling between systems, RMs need unified workspaces that bring everything together — client activity, document vault, meeting facilitation, and portfolio tracking — in one place. Real collaboration happens when RMs can securely share investment ideas, exchange documents, and message clients through familiar communication channels.

Rigid workflows rarely support the level of personalization private banking demands. Client and RM collaboration needs to be intuitive and adaptable, designed around how people actually engage.

3. Agentic AI that elevates the human touch

RMs won’t succeed if they’re the only ones doing the heavy lifting, constantly stretching their days just to keep up. They need intelligent assistants that remove complexity, automate routine tasks, and bring relevant insights directly into their flow of work

By orchestrating workflows like meeting preparation, product recommendations, or client outreach, AI agents can offload manual tasks and reduce time spent on operational overhead. These systems pull from structured internal knowledge, regulatory policies, market data, and portfolio analytics to surface contextual insights and next-best actions, without requiring RMs to become prompt engineers.

One agent may flag compliance considerations, another might suggest timely client interactions based on market shifts or portfolio composition. Together, they replicate the behind-the-scenes support an RM would typically coordinate manually — but faster, and with greater consistency. Crucially, the RM remains in the lead. These tools are designed to augment their expertise, not replace it, empowering them to focus on building stronger client relationships.

4. Actionable metrics

RMs should be supported with dashboards that bring together real-time insights into client sentiment. Relationship health indicators, such as engagement frequency, client feedback, and progress toward shared financial goals, should become part of the workflow.

These kinds of metrics not only provide clarity to the bank but give RMs themselves a sense of where and how they can make the most impact. With the right tools, they can continuously prioritize, act, and advise based on what matters most to their clients.

5. Cultivating ownership at the front line

Relationship managers are essentially entrepreneurs within their banks. They own client relationships, coordinate with specialists, and deliver results.

This is why, beyond just handing over the tools, it’s crucial to help relationship managers grow as professionals — whether that’s training in digital collaboration, guidance on sustainable investing, or tools for family governance. A culture that nurtures this ownership is key.

6. A platform built for real scale

Modern wealth platforms go far beyond surface-level interface improvements. They’re built to support the full private banking journey — from onboarding and lending to advisory, compliance, and day-to-day servicing — underpinned by an architecture that enables consistency, speed, and scale.

It’s why Deloitte identified the platform approach as a key strategy for cutting costs, speeding up time-to-market, and making costs more flexible.

Time to double down on the hybrid model

Private banking is under pressure, but it’s also full of potential. What makes this industry special — trusted human relationships — doesn’t need to be sacrificed in a digital world. In fact, it can be enhanced.

By equipping relationship managers with AI-powered support, unified tools, and smarter operating models, private banks can leverage the full value of their front line. And when RMs are empowered to be true partners, not just administrators, everyone wins: the client, the bank, and the relationship itself.

Backbase delivers this unified foundation, empowering relationship managers with modern workspaces, intelligent support, and real-time visibility into every stage of the client lifecycle. It’s a purpose-built approach to private banking that honors the white-glove tradition while future-proofing the business.