Introduction

This chasm between what SMBs need and what many banks provide has ignited a battle for the primary customer relationship. The opportunity is significant, and the risk of standing still is real. To stay relevant, banks must evolve beyond siloed products into a single, intelligent platform, forward-thinking banks can become truly indispensable.

The rise of customer dynamism: a new challenge

The new challenge isn't just nimble fintechs; it's the dawn of intelligent, automated financial management. A 2025 analysis from McKinsey, warns that AI agents are poised to make sophisticated financial decisions on behalf of customers. These agents will relentlessly seek out the best value, the most efficient experience, and the most useful tools, regardless of the provider.

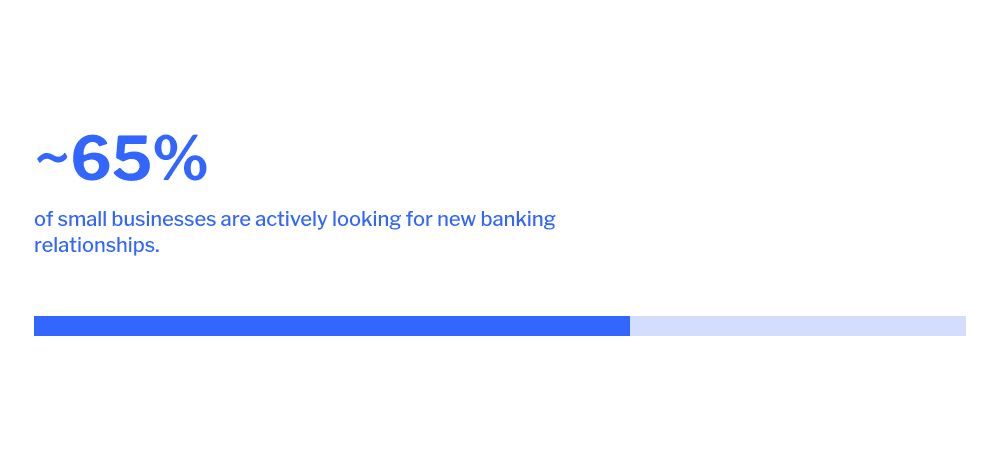

For banks, this creates a high-stakes environment where the quality of the digital experience is paramount. Cornerstone Advisors found that a staggering two-thirds of small businesses are actively looking for new banking relationships, with the primary driver being the search for better digital tools, especially customized cash flow management.

In this environment, banks that settle for “good enough” will be left behind.

This reveals a crucial distinction.

The current disconnect in the SMB banking market is not a failure of brand or a deficit of trust; it is a failure of technological capability and product vision. SMBs want their bank to be their all-in-one financial hub, but most institutions have been constrained by legacy systems and a product-siloed mindset, preventing them from delivering the unified digital experience their clients demand.

The challenge, therefore, is not an insurmountable one of changing customer perception. It is a solvable, albeit complex, problem of technological execution and strategic reorientation. The bank that successfully bridges this gap will not be pushing against the tide of customer preference but flowing with it, meeting a clear and present demand that its competitors are currently ill-equipped to satisfy.

What SMBs demand in the AI age

To win in this new landscape, banks must meet a radically new set of expectations. A 2025 report from HFS Research, conducted with partners like Accenture, stresses that commercial and SMB banking clients now demand a "360-degree view of working capital" and "real-time everything." They are no longer satisfied with lagging, historical data; they expect predictive insights and embedded services that work as fast as they do.

How banks can win: the untapped advantage of trust

Despite this glaring service gap, traditional banks possess a powerful, yet largely underutilized, strategic asset: trust. In an increasingly crowded and fragmented digital landscape, SMBs are actively searching for a central, reliable partner to help them navigate the complexities of financial management.

They are not inherently seeking to assemble a portfolio of niche fintech applications; they are seeking simplicity and consolidation from a provider they already know and trust.

Data is clear: the market is ready for change

The scale of this latent opportunity is immense.

Research found that 51% of businesses would prefer to obtain value-added services, such as data dashboards and credit checks, directly from their traditional bank.

This preference becomes even stronger for core financial workflows, with the figure rising to nearly 60% for features like real-time payments and bill payment solutions. SMBs are, in effect, asking their banks to step up and play a more significant, integrated role in their business lives.

This translates into a clear set of demands for the banking platform to become their primary financial partner:

- Predictive cash flow intelligence: Moving beyond historical reporting to offer AI-driven forecasts that can anticipate shortfalls and identify opportunities for idle cash.

- A unified financial dashboard: A single, customizable view of all financial accounts and services(including those from third-party providers)to eliminate the need to toggle between multiple apps.

- Embedded and automated workflows: Deeply integrated tools for accounts payable/receivable, payroll, and expense management that automate reconciliation and reduce manual work.

How banks can deliver unified, AI-powered SMB banking with Backbase

Banks struggle with fragmented legacy data. Celent's report, "Small Business Digital Banking Platforms: North America Edition," highlights the move to unified platforms.

Backbase's AI-powered Banking Platform was a "Luminary" in this report, receiving XCelent awards for Advanced Technology and Breadth of Functionality. Its robust UI and 400+ pre-built journeys deliver customizable, segment-based experiences for SMBs. This platform champions a growth-centric, AI-powered banking model, shifting from a closed, product-focused approach to an open, customer-centric one.

Launch, scale, and innovate faster

With Backbase, banks can serve small-business clients with end‑to‑end, beyond‑banking journeys — from rapid digital onboarding and loan origination to payroll, invoicing, and proactive cash management — within a single, branded experience. The payoff is deeper primary relationships, higher lifetime value, and a lower cost to serve.

Launch and scale faster with pre‑integrated journeys, certified connectors, and modular components. Add new capabilities without multi‑year programs and keep control over risk, data, and experience, delivering beyond-banking services like:

- Cash‑flow forecasting & insights: 7/14/30‑day projections, scenario planning, and actionable alerts that can trigger in‑flow financing when needed.

- Liquidity management: automated sweeps, just‑in‑time funding, and interest optimization across accounts and entities.

- Virtual accounts: sub‑ledgers for projects or departments, segregated receivables, and automated reconciliation to the GL.

- Expense and invoice management: ingest and classify bills, route approvals, schedule payments; issue e‑invoices with embedded payment; reconcile automatically.

External account aggregation: connect accounting, payroll, commerce, and other banks to provide a unified view with granular entitlements.

Become the command center for small businesses

Banks can either provide the central, intelligent platform that SMBs use to run their entire business, or they risk being relegated to a commoditized utility, providing back-end services while another company owns the valuable customer relationship.

By unifying customer data and leveraging a modern engagement platform, banks can offer proactive, personalized advice that builds unbreakable loyalty. Banks can segment customers with precision and anticipate their needs, becoming the trusted strategic partner they need to navigate the complexities of growth. The businesses that power our economy deserve more than just a bank; they deserve a command center.