Why is it important to look at all your options?

- Legacy platforms often suffer from outdated front ends, vendor lock-in, limited or no mobile apps, and slow or fragile integrations. These hold growth back and increase overhead costs.

- By adopting a platform that supports progressive modernization (headless architecture, incremental upgrades) you reduce risk, avoid big-bang failures, and retain continuity for customers and operations.

- Future-ready technology partners integrate speed and simplicity, with plug-and-play connectors, standardized APIs, and expanding fintech marketplaces. This makes it easier to connect core systems, CRMs, and third-party fintechs without the cost and complexity of custom builds.

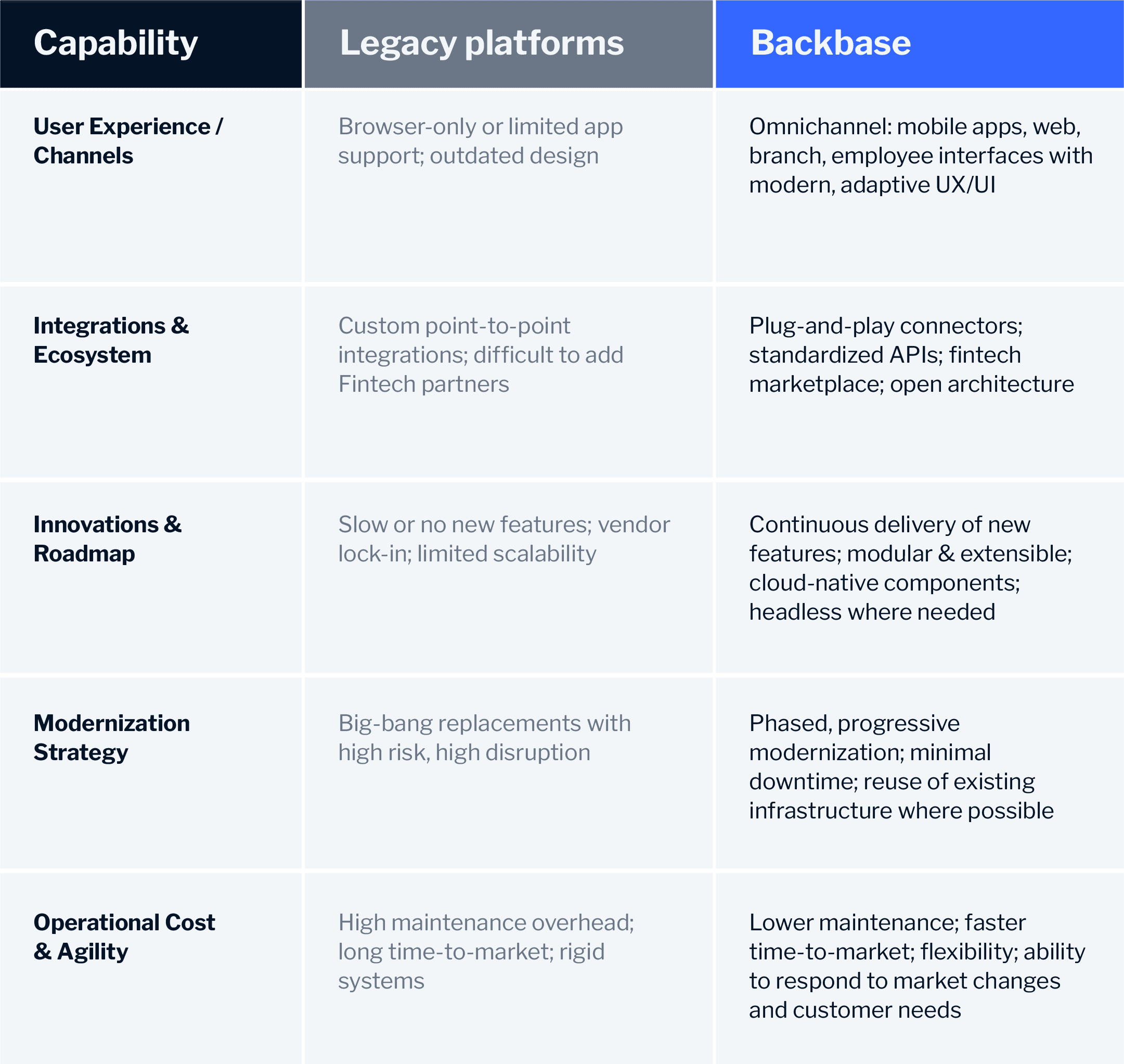

Comparison: Legacy platforms vs. Backbase

Here’s how legacy technology stacks compare to the capabilities of modern digital platforms

How can banking leaders make the change?

If I were advising a bank or credit union evaluating legacy platforms vs modern alternatives, here are the steps I’d recommend:

- Audit what’s working now: Where are your biggest bottlenecks, (e.g., mobile support, integrations, UX, or product launches)?

- Map the journey vs destination: Identify small, high-impact modernization moves (e.g. mobile app, onboarding, integrations) rather than trying to replace everything all at once.

- Choose a platform with modular, open architecture: One that lets you plug in fintechs, build or customize as needed, and scale without redoing foundational pieces.

- Prioritize customer & employee experience: Modernization should free up resources to focus on what matters for end users.