Introduction

As the digital banking experience matures, retail banks are facing a familiar challenge: how to stand out when every app offers the same transactional basics. Checking balances, paying bills, and transferring money are table stakes. What customers are looking for now goes beyond function — they want support in achieving their life goals, with financial services helping them take the right steps forward.

Banks have an opportunity to meet that demand by offering smarter personal finance and digital investing experiences. Done right, these tools help banks increase loyalty, grow share of wallet, and generate new revenue streams, all while genuinely improving customers’ financial wellbeing.

The rising demand for financial guidance in digital banking

What’s changing is expectation: people want more from their banks than efficiency. They want relevance and guidance to make confident financial decisions and achieve their goals. And increasingly, they want tools that help them feel more financially in control.

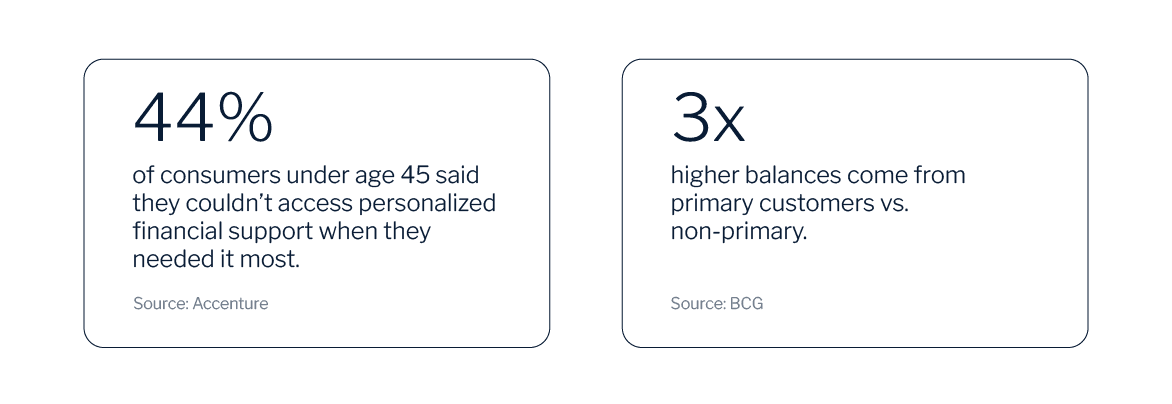

This demand isn’t confined to affluent clients; younger customers, freelancers, families all are navigating complexity. According to an Accenture report, 44% of consumers under age 45 said they couldn’t access personalized financial support when they needed it most.

Many are under-served by legacy wealth tools or siloed personal finance apps. Retail banks, with their reach and trust, are uniquely positioned to support them, both digitally and through human expertise.

Bringing customer insights to life

BCG revealed that primary customers (those with 10+ monthly transactions and recurring payments) deliver 3x higher relationship balances than non-primary ones. In short: when banks provide contextual, personalized value, customers engage more — and stay longer.

That value isn’t created by digital tools alone; it comes to life when insights guide meaningful human support. Imagine a customer service representative helping with a routine query and seeing that the customer is falling short of a savings goal. With a complete view of that customer’s finances, they can offer an on-the-spot budget review or, for example, suggest an automated savings plan.

Banks can make these tailored experiences happen with:

- Automated savings features that encourage consistent deposit growth, strengthening both customer finances and the bank’s balance sheet.

- AI-powered spend insights that give customers next-best actions and equip employees with conversation starters to add value.

- Goal-based financial planning that helps customers act on their priorities while enabling advisors to proactively suggest relevant products.

- Integrated investing journeys that offer customers the right tools and guidance, whether self-directed or through an advisor.

By helping customers feel more in control of their financial lives, banks build stronger relationships and secure their place at the center of every important financial decision.

Personalization by design

Delivering these kinds of experiences starts with personalization. It has long been the holy grail for retail banks — essential for relevance, but historically difficult to scale. Manually creating tailored experiences for every customer type is costly, slow, and hard to scale. With access to data and AI, that changes.

Today, banks can deliver segment-aware, AI-enabled experiences that feel individually tailored, without increasing operational complexity. With intelligent defaults and dynamic content based on factors like life stage, income range, behavioral patterns, and financial goals, banks can deliver personalized journeys at scale.

For example:

- A young professional might see budgeting tools, credit score insights, and first-time investing options, while employees can guide them toward starter portfolios or credit-building products.

- A freelancer could receive variable income forecasting, automated tax-saving prompts, and savings plans adapted to irregular cash flow, with branch staff ready to advise on cash management strategies.

- A family may access shared budgeting tools, joint savings pockets, and educational features for children like digital allowances and financial literacy tips.

These differentiated experiences, beyond being nice-to-haves, are real business drivers. BCG data shows that customers with a primary banking relationship (PBR) tend to log in more than 30 times per month. These deeper relationships contribute to strong retention, as PBR customers exhibit much lower levels of hard attrition (less than 2–3%).

When both digital journeys and employee interactions are informed by the same data, every touchpoint becomes an opportunity to strengthen the relationship.

Adding value with embedded investing

Investing is a natural extension of this shift; yet many banks still treat it as an add-on, or even outsource it entirely. That creates friction, fragments the experience, and drives customers to fintechs offering smoother journeys.

What’s changing is accessibility. Today’s customers expect to invest like they order food: intuitively, instantly, and with just the right amount of guidance. Banks that offer embedded investing within the same app customers use to spend and save can:

- Support first-time investors with low-barrier entry points

- Offer goal-based or thematic portfolios aligned to user interests

- Combine saving, planning, and wealth growth in one cohesive journey

Accenture research shows that over 30% of revenue from core banking products (like payments, personal loans, and credit cards) now comes through non-bank third parties, and this share is expected to keep growing.

The payoff is greater share of wallet, more monetizable interactions, and stickier customer relationships. And because investing becomes a part of the everyday experience instead of a separate destination, banks stay at the center of their customer’s financial life.

Make the most of the strategic opportunity for retail banking

At a time when margins are tightening and product commoditization is accelerating, customer experience is the new battleground. Personal finance and investing are proving to be high-impact areas — for both product expansion and strengthening everyday customer relationships.

To help banks accelerate this transition, Backbase offers an AI-powered banking platform that brings these journeys to life. Banks can:

- Launch intuitive personal finance tools, including spend categorization, budgeting, and real-time financial health insights.

- Offer goal-based saving and investing, enabling customers to link life goals to smart, guided financial actions.

- Embed investing directly into the app, with support for robo-advisory, multi-asset trading, and portfolio tracking.

- Deliver AI-powered recommendations and nudges, from contextual saving prompts to next-best investment offers.

- Tailor experiences by segment, so each user sees tools, themes, and journeys aligned to their needs and lifestyle — from students to families to mass affluent.

Retail banks have a real opportunity to lead with experiences that customers truly value. By offering smarter personal finance and investing journeys, they can turn everyday engagement into deeper relationships, unlocking new sources of growth along the way. Now’s the time to make this change.