Why is it important to look at all your options?

- Legacy platforms often suffer from outdated front ends, vendor lock-in, limited or no mobile apps, and slow or fragile integrations. These hold growth back and increase overhead costs.

- By adopting a platform that supports progressive modernization (headless architecture, incremental upgrades) you reduce risk, avoid big-bang failures, and retain continuity for customers and operations.

- Future-ready technology partners integrate speed and simplicity, with plug-and-play connectors, standardized APIs, and expanding fintech marketplaces. This makes it easier to connect core systems, CRMs, and third-party fintechs without the cost and complexity of custom builds.

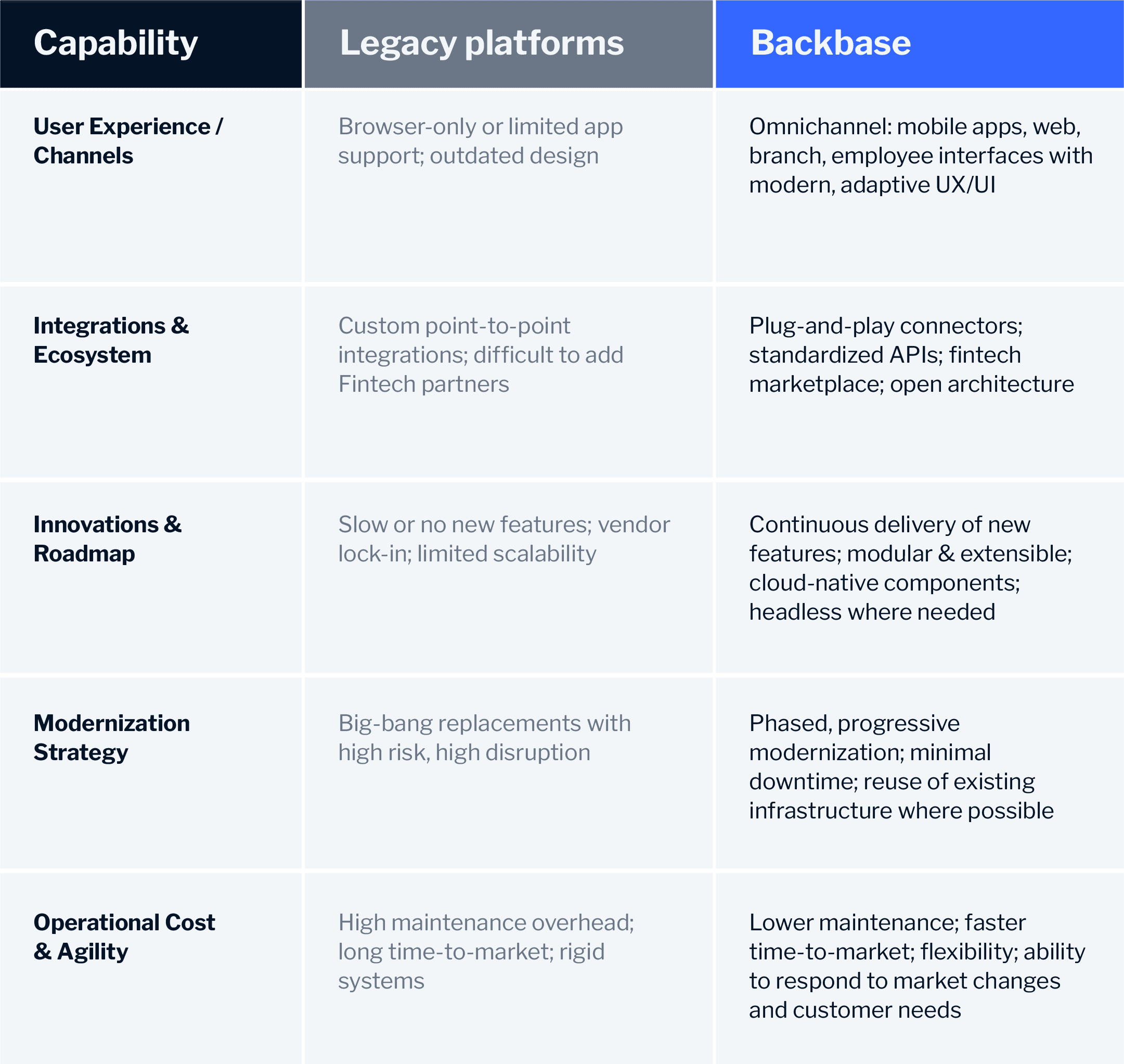

Comparison: Legacy platforms vs. Backbase

Here’s how legacy technology stacks compare to the capabilities of modern digital platforms

How can banking leaders make the change?

If I were advising a bank or credit union evaluating legacy platforms vs modern alternatives, here are the steps I’d recommend:

- Audit what’s working now: Where are your biggest bottlenecks, (e.g., mobile support, integrations, UX, or product launches)?

- Map the journey vs destination: Identify small, high-impact modernization moves (e.g. mobile app, onboarding, integrations) rather than trying to replace everything all at once.

- Choose a platform with modular, open architecture: One that lets you plug in fintechs, build or customize as needed, and scale without redoing foundational pieces.

- Prioritize customer & employee experience: Modernization should free up resources to focus on what matters for end users.

The hidden cost of legacy technical debt in banking

Most banks know legacy systems are expensive. Few have quantified exactly how expensive.

Banks spend approximately $600 billion on technology annually - with the majority consumed by maintaining existing legacy infrastructure rather than building new capabilities. lThat leaves less for innovation, new products, and competitive differentiation.

The cost compounds in three ways most finance teams don't fully capture.

Direct maintenance cost. Legacy systems require specialized engineers who understand decades-old code. That talent is scarce and expensive. Every year, the pool shrinks as those engineers retire.

Opportunity cost. Every dollar spent maintaining a mainframe is a dollar not spent on AI, new products, or customer experience improvements. Banks running modern architecture ship features in weeks. Banks on legacy systems ship in quarters - if at all.

AI readiness cost. This is the newest and fastest-growing dimension. Banks deploying AI agents discover quickly that the models work fine. The foundation underneath them doesn't. Agents need unified customer context, shared data, and a coordinated execution layer. Legacy systems provide none of these. Every AI initiative on a fragmented legacy stack requires custom integration work from scratch - multiplying the cost of every deployment.

The result is a compounding disadvantage. Banks that modernized early are now deploying AI across their entire frontline. Banks still on legacy systems are paying twice - once to maintain the old infrastructure and once to build custom bridges for every new capability they try to deploy on top of it.

Why AI makes legacy debt more urgent, not less

For years, banks managed legacy technical debt as a known cost of doing business. Painful but stable. The AI era has changed that calculation entirely.

AI agents need three things to operate reliably in a banking environment. Unified customer context - a single view of the customer that every agent, employee, and workflow operates from. Governed decision authority - explicit policies that define what any actor is allowed to do, under what conditions, with a full audit trail. A coordinated execution layer - the ability to act across systems without custom-built pipelines for every workflow.

Legacy architecture provides none of these by design. Core banking systems, CRM platforms, payments rails, and risk engines each hold their own version of the customer - updated on their own schedule, with no shared state. When you deploy an AI agent on this foundation, it operates on partial information, follows inconsistent rules, and writes back to different systems with different versions of the truth.

The result is not AI transformation. It is AI theater - pilots that look promising in a controlled environment and break down the moment they touch production scale.

This is why the banks moving fastest on AI are not the ones with the biggest AI budgets. They are the ones that fixed the foundation first. Every dollar spent on modernization now is worth multiples in AI deployment speed later. The architecture you build today determines what your bank can do in 2027 and beyond.

Frequently asked questions about banking legacy modernization

What is banking legacy technical debt?

Banking legacy technical debt is the accumulated cost of maintaining outdated technology systems that were built for a different era. It includes the direct cost of keeping old infrastructure running, the opportunity cost of development resources consumed by maintenance rather than innovation, and the growing cost of bridging fragmented systems every time a new capability is deployed. For most banks, legacy technical debt consumes 70-80% of the annual IT budget.

Why do banks struggle to replace legacy systems?

Legacy systems are deeply embedded in banking operations. They handle critical functions like transaction processing, account management, and regulatory reporting. Replacing them carries significant operational risk. The challenge is not technical willingness - most banks understand the problem clearly. The challenge is finding a path to modernization that does not require a big-bang replacement that takes years and risks operational continuity.

What is progressive modernization in banking?

Progressive modernization is the approach of modernizing one domain at a time rather than attempting a complete system replacement. Banks start with the highest-value workflows - onboarding, loan origination, dispute resolution - and modernize those first while leaving the underlying core systems intact. Each domain modernized adds to the same operating model. The architecture compounds over time without the risk of a single large-scale migration.

How does legacy technical debt block AI adoption in banking?

AI agents need unified customer context, governed decision authority, and a coordinated execution layer to operate reliably. Legacy systems fragment all three. Customer data lives in separate systems with separate definitions. Policies are enforced inconsistently across channels. Actions require custom integration work for every new use case. Banks attempting to deploy AI on fragmented legacy architecture consistently find the models are not the problem - the foundation underneath them is.

What is the difference between core banking replacement and legacy modernization?

Core banking replacement involves replacing the system of record - the ledger that holds account balances, transaction history, and product data. This is a multi-year, high-risk program that most banks approach with caution. Legacy modernization takes a different approach - placing a coordination layer above the existing core that handles customer journeys, AI agents, and frontline operations without touching the ledger. The core stays intact. The operational layer above it modernizes progressively.

How long does banking legacy modernization take?

With a progressive approach - modernizing one domain at a time using pre-validated solutions - banks can have a first domain live in production within months. The full transformation to a unified frontline typically takes 24-36 months across all domains. The key difference from traditional transformation programs is that value is delivered continuously throughout the journey rather than at the end of a multi-year project.