Introduction

Last time, we discussed 3 considerations for the responsible adoption of AI in banking, and we hope it helped to allay your concerns about this new-generation tech. In this blog, we cover the top 5 business applications of AI in banking — the ones with the most immediate impact on operations, cost, and growth.

Adoption will vary based on your regulatory environment, market, and resources — but these are the applications worth prioritizing.

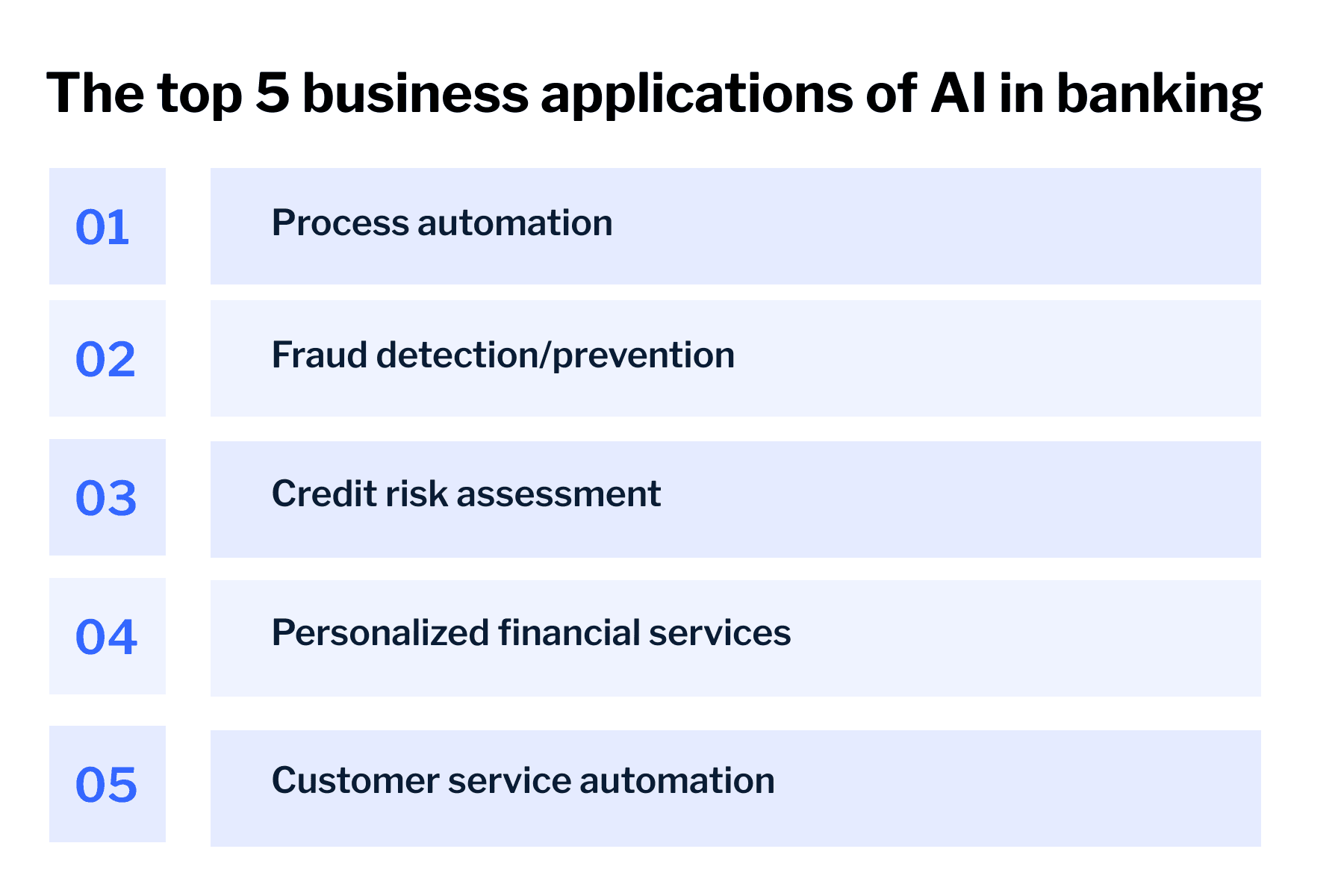

1. Process automation

AI automates repetitive banking tasks by combining robotic process automation (RPA) with machine learning — handling both rule-based workflows and complex, data-driven decisions. The result: fewer errors, lower operational costs, and employees freed up for higher-value work.

The tasks ripe for automation include:

- Account reconciliation: AI matches transactions and flags discrepancies in real time, eliminating manual review cycles.

- Document processing: Intelligent document recognition extracts and validates data from contracts, applications, and statements automatically.

- Compliance reporting: AI continuously monitors activity and generates audit-ready reports, reducing regulatory risk.

Accenture estimates banks could automate up to 60% of routine data collection and processing tasks for tellers alone — and that's just the starting point.

2. Fraud detection/prevention

AI is already able to pick up on things that humans simply can't, and this can go a long way towards the early detection — and hopefully prevention — of fraud. By using advanced machine learning algorithms trained on large sets of historical transaction data, your bank will be able to identify abnormal patterns.

And when you couple this with real-time monitoring systems, this becomes even more compelling. By leveraging AI, you'll start to minimize financial losses and even boost customer trust in the process.

3. Credit risk assessment

Credit scoring takes a long time due to all the underlying factors that must be analyzed, from customer behavior to transaction history and more. But AI will enhance not only the speed of the process, but also the accuracy, due to its ability to speedily review a broader set of data.

Thanks to predictive models, your bank will be able to generate more personalized, dynamic risk profiles that will help you make better lending decisions and reduce the risk of defaults.

4. Personalized financial services

AI will make personalization practically effortless, allowing your bank to offer tailored financial services and products at scale. By using recommendation engines to analyze spending habits, income, life events, and more, you'll be able to suggest the right investment strategy, for example, to the right person at exactly the right time. And that will go a long way towards improving your ability to cross and up-sell.

5. Customer service automation

Most customer queries are repetitive. AI-powered chatbots use natural language processing (NLP) to handle common requests instantly and route complex issues to human agents.

The operational wins are immediate:

- Faster response times: Customers get answers in seconds, not minutes.

- Lower operational costs: Fewer agents needed for high-volume, low-complexity queries.

- Higher satisfaction scores: Consistent, accurate responses build customer trust at scale.

Did you know that

McKinsey estimates that AI tech could help deliver up to $1 trillion of additional value to global banks each year, of which revamped customer service is a huge part.

Frequently asked questions

What AI applications deliver the most value for banks right now?

Process automation and fraud detection deliver the fastest ROI — they directly reduce operational costs and financial losses while requiring less organizational change than customer-facing AI deployments.

Is AI in banking ready for production deployment?

Yes — for well-defined use cases like transaction monitoring, document processing, and credit scoring, AI is already running in production at major institutions globally.

How does AI improve credit risk assessment in banking?

AI-powered predictive models analyze a broader set of variables — including transaction history, behavioral signals, and external data — faster and more accurately than traditional scoring methods, reducing default risk and improving lending decisions.

The top 5 customer applications

Next up: the top 5 customer applications of AI in banking — covering fraud protection, personalized advice, and more. Then, don't miss our interview with Chris Shayan, Backbase's Head of AI and former CTO of TechComBank, sharing his 3 tips for getting AI into production at your bank.

For more information, check out our Banking Reinvented podcast, where Backbase Founder/CEO Jouk Pleiter dissects similar topics alongside Tim Rutten, EVP/CMO, and other digital leaders. Stay tuned as they chat about everything from progressive modernization to decomposing your bank's complexity.