Introduction

Private banking is entering a new phase — one defined not by access or exclusivity alone, but by a client's expectation for continuity, context, and control across every dimension of their financial lives.

Today's HNW individuals and families want their financial institutions to understand their broader needs: planning, lending, liquidity, lifestyle, and legacy. They want that understanding delivered consistently across digital and human channels.

This article examines what's changed in client expectations, where private banks are falling short, and what a true holistic wealth proposition looks like in practice.

A structural change in wealth management

Client expectations in private banking have changed more in the past five years than in the two decades before them. HNW individuals no longer evaluate their bank on discretion and access alone. They expect continuity, context, and control — across every channel, every service, and every stage of their financial lives.

A significant 55% of HNWIs now value robust digital channel capabilities when choosing a private bank or wealth manager. That presents serious challenges, including meeting the demand for digitized services and providing a wider range of sophisticated advice.

Clients want guidance that goes well beyond investment advice. Private banks must now cover the full spectrum of a client's financial life:

- Wealth planning: Structuring assets to support long-term goals across generations.

- Tax and legal advice: Navigating complex cross-border and multi-entity arrangements.

- Inheritance and estate planning: Ensuring smooth wealth transfer with minimal friction.

- Philanthropic strategy: Aligning giving with family values and legacy objectives.

Delivering this requires private banks to rethink both their proposition and their operating model.

Digital channels aren't optional anymore. Banks that lack them aren't just behind on experience — they're losing clients to firms that have already moved.

Where private banks struggle

Discretion remains critical. But clients now expect that discretion to extend across mobile dashboards, instant RM access, and the ability to manage complex portfolios and legal structures with ease.

This is a marked departure from the engagement model that many firms still rely on. It's putting pressure on banks to reconsider how they organize their propositions, enable their RMs, and integrate their technology. Current challenges include:

- Service fragmentation, with clients navigating disjointed tools and teams to manage different elements of their finances.

- Inadequate digital interfaces, which fail to reflect the sophistication clients experience in other parts of their lives.

- Manual RM workflows, which reduce both responsiveness and time spent on strategic engagement.

How to move forward? Defining a holistic wealth proposition

A holistic approach to wealth management does not mean offering every service in every channel. It means integrating core elements — banking, investing, lending, planning — into a coherent, unified experience that reflects a client's financial reality.

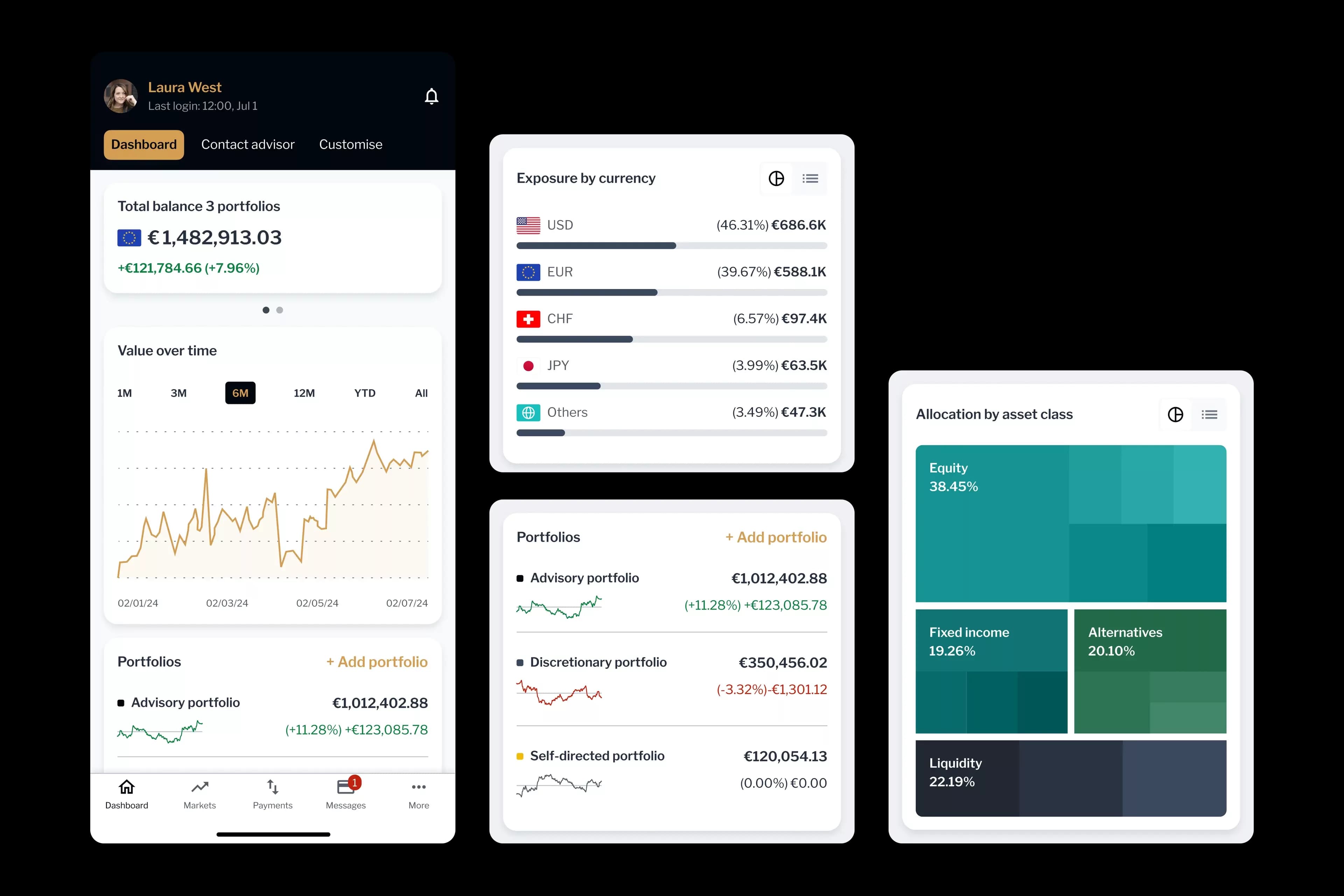

1. A unified financial view across the client's full balance sheet

For many private clients, wealth is anything but centralized. Holdings are spread across multiple custodians, accounts, asset classes, and legal structures — often across multiple jurisdictions. The result is a fragmented picture that even experienced clients struggle to navigate.

A holistic proposition requires that banks take responsibility for restoring clarity. That means building infrastructure that consolidates and contextualizes financial data across internal systems and third-party sources to offer a real-time, comprehensive view of a client's total wealth.

FAQ: Why do HNW clients need a unified financial view?

Q: Why is a unified financial view important for private banking clients?

A: HNW clients typically hold assets across multiple custodians, structures, and jurisdictions. Without a consolidated view, they — and their relationship managers — are making decisions with incomplete information.

Clients should be able to explore how changes in one area, such as a refinancing event or asset sale, affect their broader financial strategy. Relationship managers, in turn, should have access to the same information to provide relevant, well-timed guidance. This shared clarity forms the baseline for trust — and lays the groundwork for more meaningful engagement over time.

2. Embedding digitally supported wealth planning into the core relationship

Private clients don't segment their financial lives the way banks do. Wealth planning, lending, and investment decisions are deeply interconnected, yet many banks treat these areas as separate functions.

This is why planning must be embedded directly into the client experience — through digital tools for scenario modeling, multi-entity structuring, and goal tracking, as well as secure collaboration spaces where clients, RMs, and third-party advisors can work together on planning outcomes.

These journeys must accommodate complexity without adding friction. For UHNW clients, that means managing a foundation, a family business, and a multigenerational trust structure — all within a single planning environment.

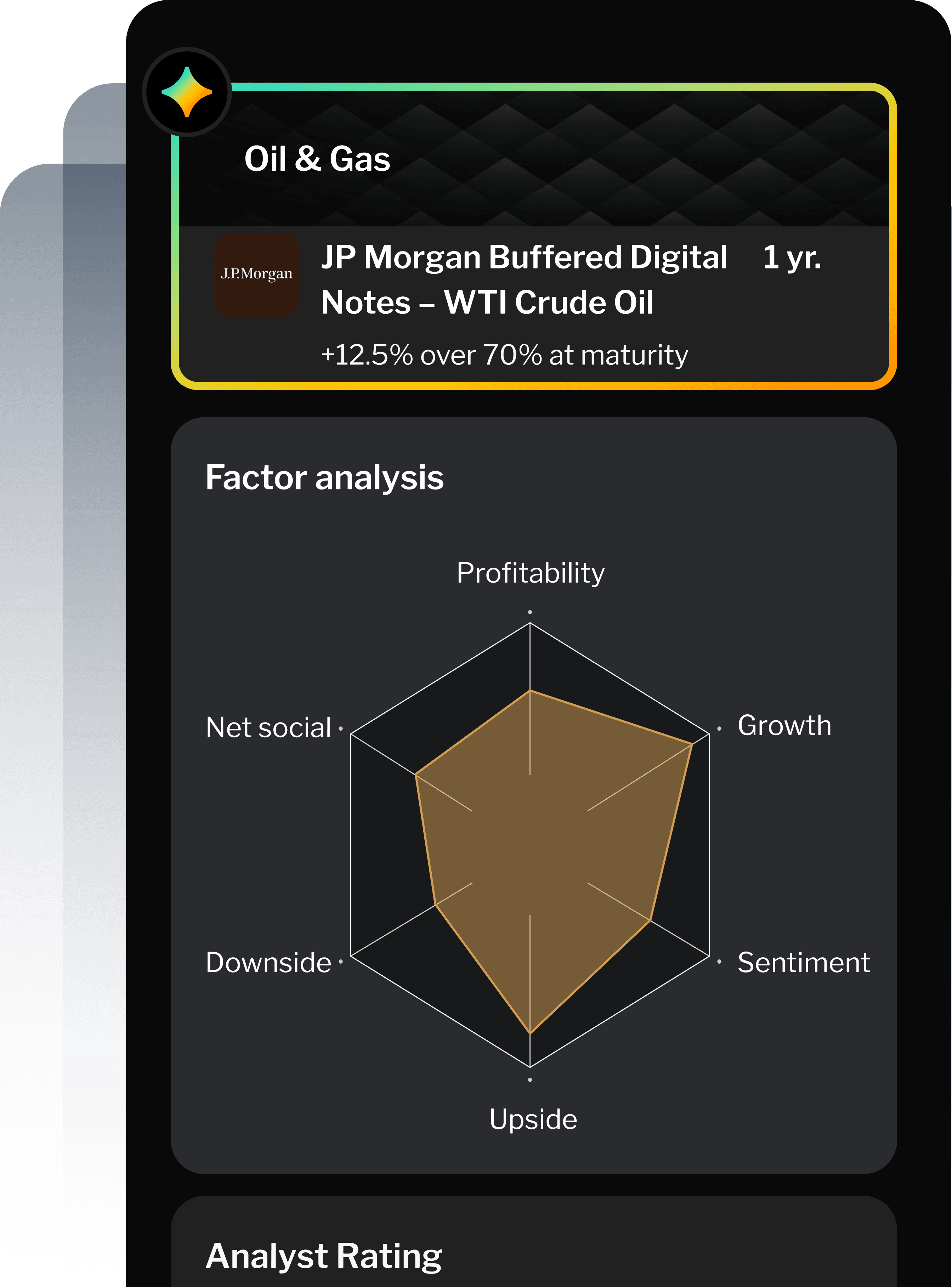

3. Turning insight into action: enabling proactive, AI-powered engagement

Even with clear visibility and structured planning, clients expect their bank to take initiative. They want their RMs to anticipate needs, highlight risks, and provide well-timed, relevant recommendations.

This is where digital enablement makes the difference. With AI-powered alerts and embedded nudges, RMs can be notified when a client's liquidity falls below a threshold, when portfolios drift out of alignment, or when a regulatory milestone approaches.

The impact is twofold: clients receive timely, personalized support, and RMs spend more time building relationships, not managing processes. This shift from reactive service to proactive engagement strengthens loyalty — and positions the bank as a trusted, strategic partner in the client's financial life.

Delivering holistic wealth management with purpose

A holistic wealth proposition isn't about offering more services. It's about making every service work together — delivered in a way that reinforces trust, transparency, and client control at every touchpoint.

For banks, that means moving beyond product-centric engagement and toward experiences that reflect the full complexity of each client's financial life. It means designing journeys that blend digital convenience with expert guidance, and equipping relationship managers to operate not as intermediaries, but as strategic partners.

Backbase helps private banks realize this vision. Our AI-powered banking platform brings intelligence into every interaction — giving RMs the tools to act decisively, and clients the experience they expect.

- Unified financial view: Consolidate data across custodians, structures, and jurisdictions into a single client picture.

- Embedded planning tools: Scenario modeling, goal tracking, and multi-entity structuring built into the core relationship.

- AI-powered RM enablement: Proactive alerts and insights that shift RMs from reactive service to strategic partnership.